The Big Picture

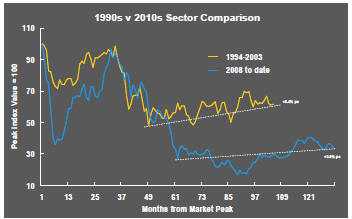

After recovering through 2010, a lengthy downtrend in sector prices between 2011 and 2015 gave way to a relatively stable trajectory similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of frequent macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability in sector prices suggests a chance for individual companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low some 90 months after the cyclical peak in sector equity prices but these conditions were reversed through 2016 and 2017 although, for the most part, sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

In the absence of a market force equivalent to the industrialisation of China, which precipitated an upward break in prices in the early 2000s, a moderate upward drift in sector equity prices over the medium term is likely to persist.

The Past Week

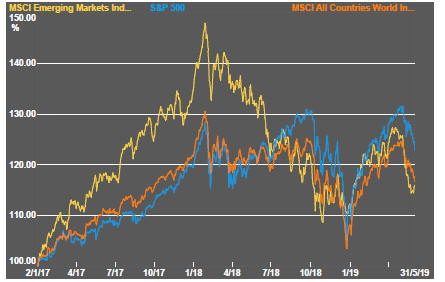

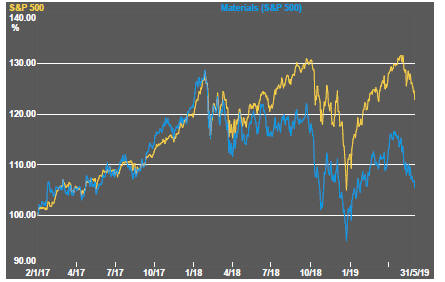

The downward trajectory in equity prices continued although, at the end of the week, emerging markets showed the first signs, perhaps temporary, of holding ground.

Aggravating already pronounced signs of weakening growth, the US president tweeted out his intention to tax goods imported from Mexico as long as the country’s government failed to co-operate in stemming the northward flow of Latin American migrants.

Trade tensions of varying degrees of significance now involve China, Europe, Japan and Mexico. The revised NAFTA agreement - the single sign of progress on the trade front for the American president - is now in disarray.

Chinese officials will now be wondering why they should bother seriously pursuing a deal if the US is so prepared to renege on an already concluded agreement which had been slated to go to legislators in the three North American countries in the past week for ratification.

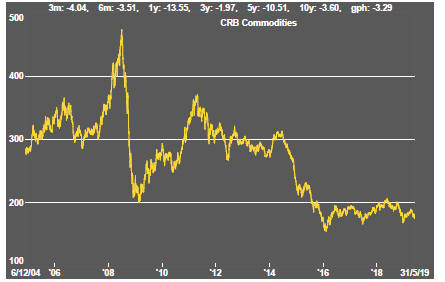

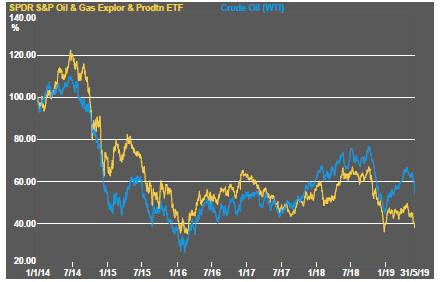

Weak crude oil prices and energy equity prices added to the downward market pressures.

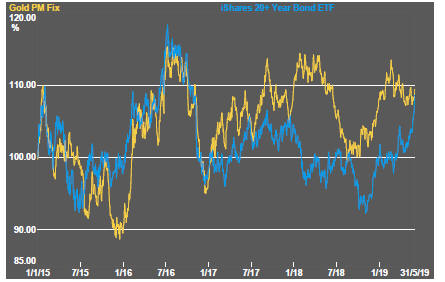

At the same time, expectations of central bank policy support for markets rose with financial market pricing reflecting expectations of multiple reductions in US rates and easier monetary conditions in Europe.

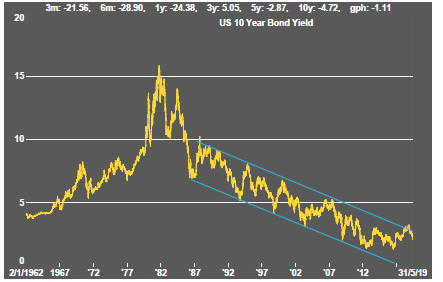

German and US bond yields pushed lower suggesting broad-based expectations of weakening activity.

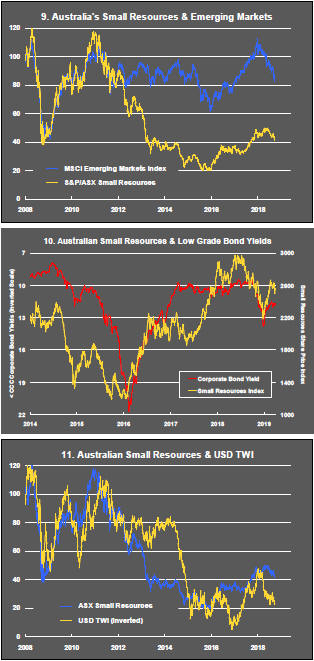

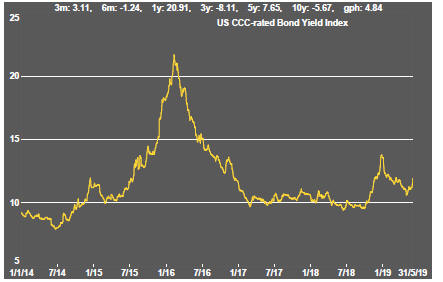

Of particular concern for the mining industry, the unfavourable spread between government and high yield corporate bond prices widened.

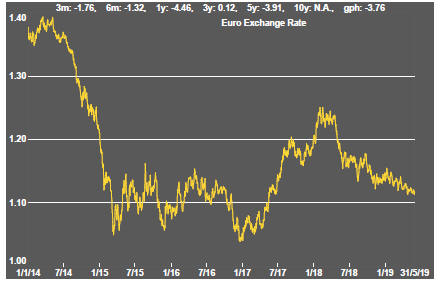

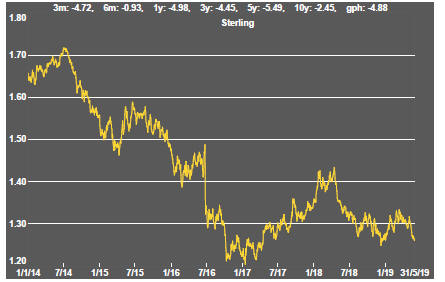

The upward trajectory of the US dollar remained an added drag on metal prices. Resource sector equity prices have continued to display unusual resilience in light of the broader macro position. Helping the headline index measures of performance has been a favourable move in iron ore prices which has benefitted the market leaders.

Gold prices reacted little to the surge in bond prices suggesting a larger move in precious metal is ahead.

Silver prices are trading more in line with industrial metals than gold as the under-performance of the former persists.

Copper prices moved lower in concert with bond yields, both implying that global growth is an important driver of market direction. Iron ore prices are breaking the broader trend in metal prices as supply disruptions benefit the Australian oriented market leaders.

The lithium sector price indicator, which includes Phase II companies, is underperforming dramatically in another sign, within a part of the market widely thought to have the best prospects, of risk aversion.

Sector Price Outcomes

52 Week Price Ranges

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.

Equity Market Conditions

Resource Sector Equities

Interest Rates

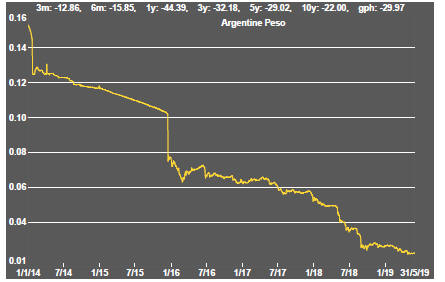

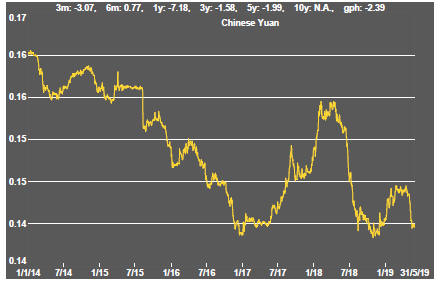

Exchange Rates

Commodity Prices Trends

Gold & Precious Metals

Nonferrous Metals

Bulk Commodities

Oil and Gas

Battery Metals

Uranium