The Big Picture

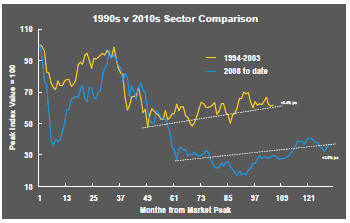

After recovering through 2010, a lengthy downtrend in sector prices between 2011 and 2015 gave way to a relatively stable trajectory similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of frequent macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability in sector prices suggests a chance for individual companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low some 90 months after the cyclical peak in sector equity prices but these conditions were reversed through 2016 and 2017 although, for the most part, sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

In the absence of a market force equivalent to the industrialisation of China, which precipitated an upward break in prices in the early 2000s, a moderate upward drift in sector equity prices over the medium term is likely to persist.

The Past Week

Equity prices largely maintained their upward trajectory although signs of momentum loss were beginning to show.

The potentially positive effects on markets of a denuclearisation deal between North Korea and the USA did not eventuate. Meanwhile, in the USA, President Trump was being assailed by his political opponents, including his former personal lawyer who testified before Congress.

More directly significant for the economic outlook, US trade negotiator Robert Lighthizer emphasised in congressional testimony how difficult a trade agreement with China would be to implement. Any near term agreement would simply be the start of a decade or longer of engagement with Chinese officials to ensure that they were wedded to the reforms being sought and promised.

Meanwhile, Fed Chairman Jerome Powell continued to emphasise the US central bank’s policy pivot, which had shored up markets, with a still stronger statement to Congress about its balance sheet runoff finishing by the end of 2019.

On the global growth front, evidence that the world had entered a period of synchronised slowdown was becoming more conclusive. China reported another month of contracting manufacturing activity. US GDP growth in the fourth quarter of 2018 was slightly stronger than expected but consistent with sub-3% outcomes. Powell, in addressing Congress, suggested that long-term growth will be anchored by low productivity outcomes and constrained by future growth in employment, matters over which the Fed had little influence, leaving growth outcomes closer to 2% and possibly lower.

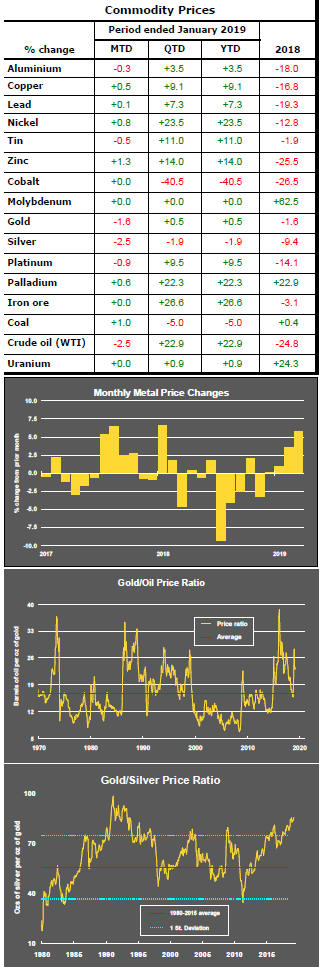

Metal prices remained surprisingly strong against the backdrop of slowing global growth. An anticipated conclusion to US-China trade discussions, with beneficial effects on Chinese economic growth, seemed to support commodity prices. A sustained cyclical turnaround would depend on China’s recent growth slowdown having stemmed from the trade dispute. If, in fact, the cause of the slowdown is a set of more deep-seated structural forces, current commodity price strength may prove a false dawn.

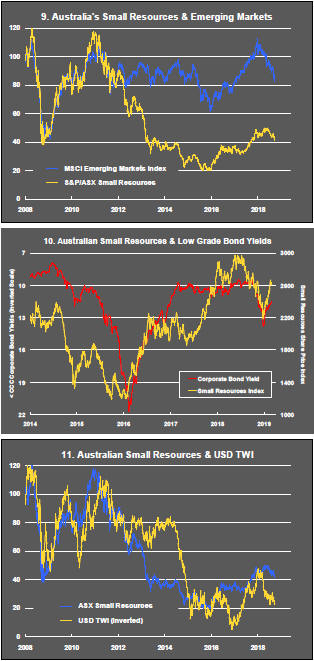

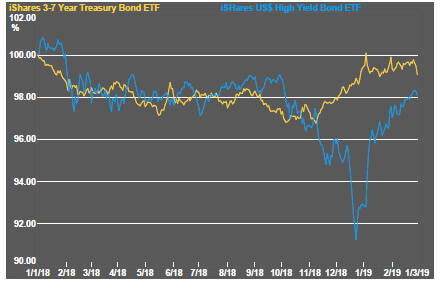

The closing gap between government bond prices and the prices of low grade corporate debt remained a favourable sign for mining industry funding.

Resource sector equity prices ended the month on slightly weaker notes than had been evident in the prior four weeks.

Currency movements generally had little impact on the sector although sterling showed strength after a series of parliamentary votes appeared to significantly reduce the chance of the UK exiting the European Union without a formal transition agreement.

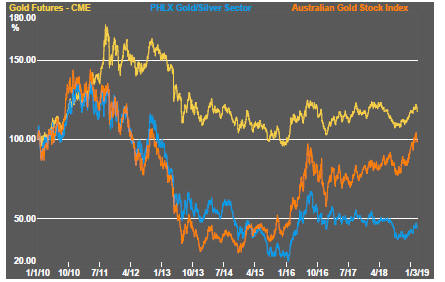

Gold prices eased back, in line with financial market prices and having failed to exceed price levels previously reached in mid 2016 and early 2018 before losing ground at those points.

The contradictory signals from copper price movements and US bond yields at the end of 2018 – both historical indicators of growth expectations - appear closer to resolution with the bond market having endorsed the weaker growth outlook implied by the copper market.

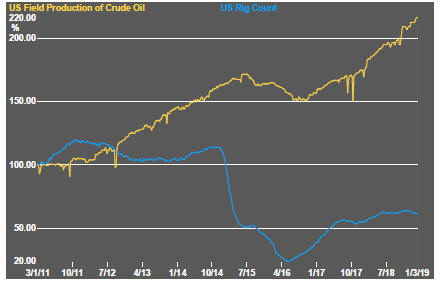

Stronger crude oil prices have not flowed into equity price indicators for oil and gas explorers and producers suggesting continuing scepticism about the sustainability of the prices being managed higher by the Saudi Arabian and Russian governments and subject to continued pressure by increasingly efficient US production.

Sector Price Outcomes

52 Week Price Ranges

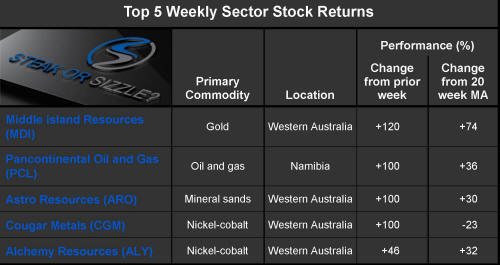

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.

Equity Market Conditions

Resource Sector Equities

Interest Rates

Exchange Rates

Commodity Prices Trends

Gold & Precious Metals

Nonferrous Metals

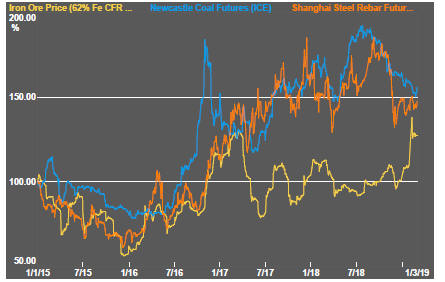

Bulk Commodities

Oil and Gas

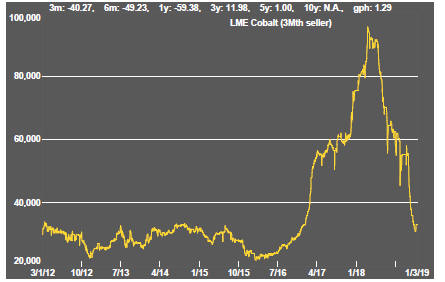

Battery Metals

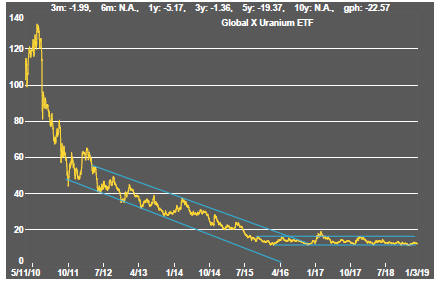

Uranium