The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

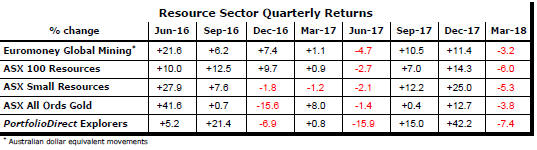

Resource Sector Weekly Returns

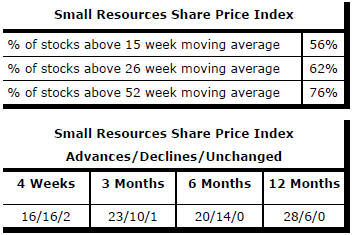

Market Breadth Statistics

52 Week Price Ranges

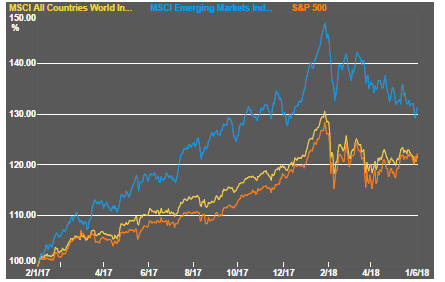

Equity Markets

Markets continued to display little positive momentum with large losses and gains alternating through the week in reaction to news about the summit between the leaders of the USA and north Korea and to changes in tone about trade negotiations netting to a modest return.

Gains at the end of the week were driven by technology stocks - as the NASDAQ and S&P 500 technology sector indices show.

The NASDAQ market neared record price levels. Smaller stocks, for which the Russell 2000 acts as a proxy, were again strong enough to set a new record level.

Russell 2000 stocks are generally regarded as having a lesser international exposure. With the US economy seemingly growing faster than other advanced market economies and large companies caught up in a potential trade war, the relative attractiveness of the smaller domestic oriented companies has improved.

The US labour market data for May released on Friday was far stronger than many had expected giving heart to investors concerned about growth. While overall wage growth remains subdued by historical standards, evidence of labour shortages and upward wages pressures are becoming more evident in several sectors.

The US administration announced during the week that tariffs would be applied to a range of metal products from Europe and Canada. Equity markets are responding less aggressively to the changes in mood over trade as many investors conclude that President Trump has continually taken disruptive positions as a way of opening new ways forward. As a consequence, the ultimate outcome is largely unknown although the broadening consensus is that Trump is likely to settle for something less, not only in trade, than his initial demands.

Resource Sector Equities

Weekly returns within the materials sector were positive with the strongest gains once again among the largest companies in the sector.

Within the Australian market, resources outperformed industrial company share prices.

Australian gold equities performed more strongly than those of its international peers.

Interest Rates

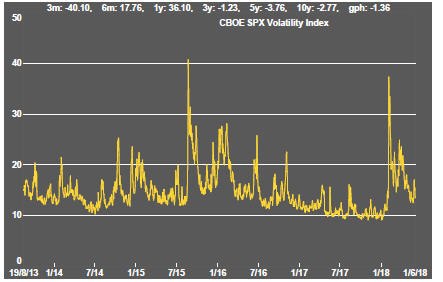

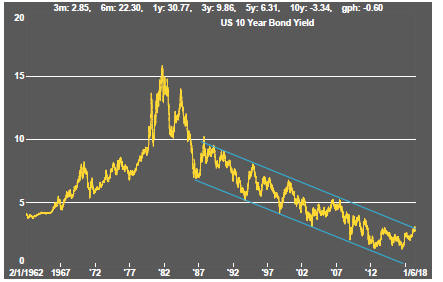

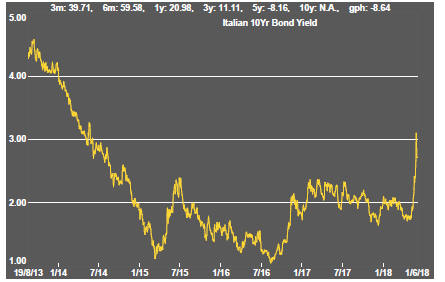

US 10 year bond yields retreated further after first breeching 3% a fortnight earlier.

The decline in yields is at odds with the relative strength of the US economy but linked to the flight to safety as a result of the Italian political impasse. German yields were also lower as Italian political parties appeared unable to form a new government. Yields reversed late in the week as disagreements in Italy were papered over in response to threats of a new election.

Although the composition of a new Italian government has been agreed, its policy positions remain a worry for European policymakers being pushed toward accepting a blowout of Italian government debt.

Importantly for the mining industry, higher risk corporate debt yields have remained at the lower end of the recent range.

Exchange Rates

The upward tendency of the US dollar persisted with a relatively strong US economy and economic and political uncertainty elsewhere.

Expectations of synchronised growth around the world which favoured a lower US dollar have been giving way to a more fractured growth outlook. Exchange rate movements have reflected these changes particularly with the onset of political instability in Italy and as the deadline for negotiating final Brexit arrangements nears.

While each of the developing market currency shifts could be attributed to the specific circumstances of the individual countries, recently higher oil prices have been a common factor among those which are oil importers such as Turkey and Argentina.

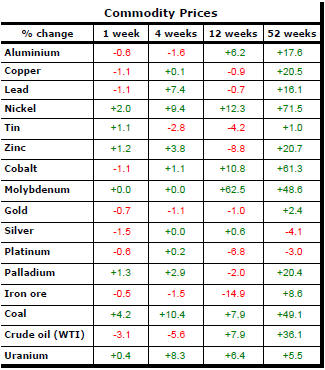

Commodity Prices

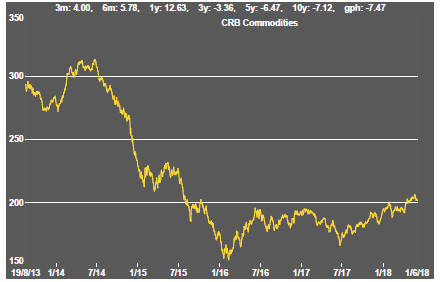

The CRB index had returned to levels last experienced in 2015. The general upswing in commodity prices had been given added impetus by stronger crude oil prices which have eased back, taking the CRB commodities index lower over the past two weeks.

Prices remain within the bounds of a cyclical trough, albeit at the upper end.

The flip side of the benefits for commodity producers and exporters of higher commodity prices is the cost pressures now being experienced by users of agricultural and raw material commodities. Reporting companies have been suggesting this as a source of margin compression.

Business surveys closely watched by central banks are showing signs of upward pressure on selling prices as a result of higher raw material prices.

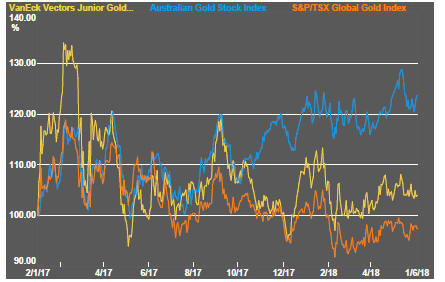

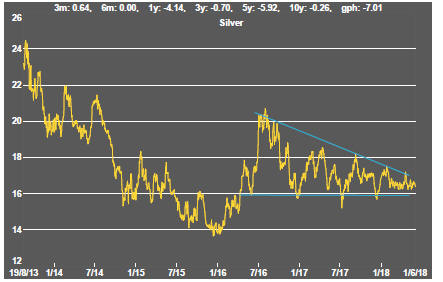

Gold & Precious Metals

Movements in precious metal prices remained muted with a noticeable lack of response in recent weeks to changes in bond yields.

Across the sector, prices appear close to a turning point as they butt up against the bounds of prior trading ranges.

The divergence in trend between Australian and north American gold related equities remains evident with US markets more aligned with a sceptical view of the near term future of precious metal prices.

Nonferrous Metals

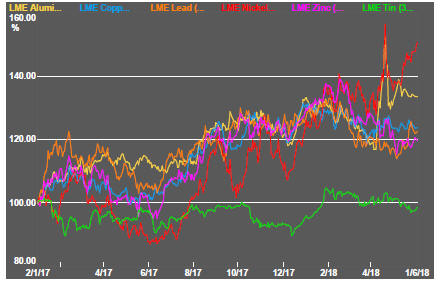

Prices of the main daily traded nonferrous metals had broken into three groups. Group one comprised those affected by US sanctions on Russian economic and political interests, namely nickel and aluminum. The second group includes those metals being driven by broader macro trends which are experiencing a loss of momentum. The third category comprises tin alone.

Nickel prices stood out in the past week with sharp gains.

The copper trading pattern shows a loss of momentum which could be restored but which is also consistent with a significant turning point. A failure of US bond yields to push higher - normally a sign of more buoyant economic conditions and consistent with rising demand for copper - would be consistent with an inflection point in the copper price trend.

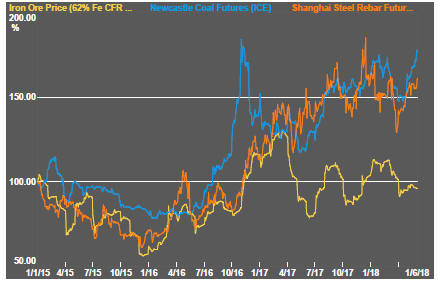

Bulk Commodities

Relatively weak first quarter Chinese GDP growth had suggested a ramp up in activity through the remainder of 2018 if China was going to meet its growth target which, in a centrally controlled economy in which leaders are trying to maintain credibility, is a reasonable assumption.

Iron ore prices have failed to reflect the ongoing expansion in manufacturing output although coal and steel prices have risen once again.

Oil and Gas

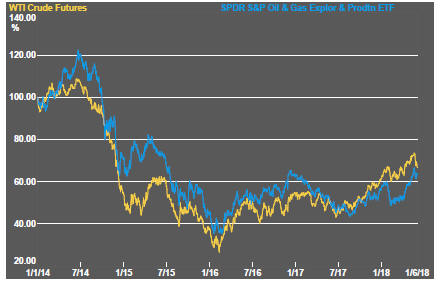

Crude oil prices had reached the highest levels in several years before breaking lower over the past two weeks.

Russian president Vladimir Putin was reported as saying that a $60/bbl oil price would be adequate and other producers had hinted at an expansion in production.

The sharp market response to the slightly more bearish tone might lead to some reconsideration of any plans to push output higher.

US production, in any event, continues to rise. US producers are able to profitably hedge anticipated production contributing to the ongoing rise in their output.

Battery Metals

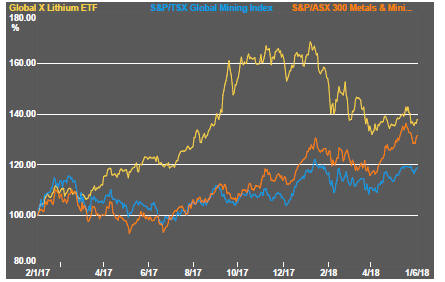

Eighteen months of rising lithium-related stock prices gave way to a period of market reassessment as a lengthy pipeline of potential new projects raised the prospect, although not conclusively, of ongoing supplies being adequate for expected needs.

Potential lithium producers have been able to respond far more quickly to market signals than has been the case in other segments of the mining industry with development prospects.

Movements in lithium related equity prices have been aligned more closely with overall sector equity prices in recent weeks.

Battery metals remain a focal point for investors with recent attention moving to cobalt and vanadium.

Doubts about a peaceful transfer of power in the Democratic Republic of the Congo (and an Ebola outbreak) has added a dimension to cobalt prices lacking in other metals caught up in the excitement over transport electrification.

In the longer term, cobalt is the most vulnerable of the battery related metals to substitution with high prices likely to stimulate research in that direction.

Uranium

The uranium sector is forming a cyclical trough as market balances slowly improve but in the absence of more meaningful signs that power utilities are prepared to re-enter the contract market to negotiate longer term needs.

Slightly higher equity prices from time to time, in the hope of improved conditions, have not been sustained but could be repeated as speculation about improved future demand ebbs and flows.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.