The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

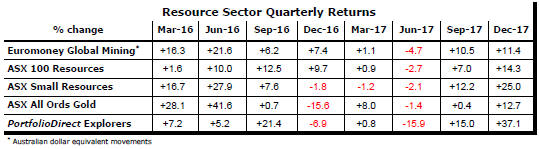

Resource Sector Weekly Returns

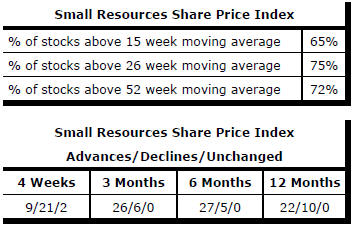

Market Breadth Statistics

Equity markets were buffeted at the end of the week following the latest US monthly labour market report showing higher than expected employment growth and an acceleration in the rate of wages increase.

While both indicators could also have also been interpreted as good for equity prices, nervousness about valuations after the recent strength of markets contributed to a highly negative interpretation.

Investors seemed to infer that higher wages growth would cause more aggressive increases in interest rates during 2018 than had been flagged previously by members of the Federal Reserve.

The broad based equity sell-off meant that the both interest rate sensitive sectors as well as those that might benefit from higher rates, such as the banks, suffered price falls.

Before Friday's labour market report, financial markets had already been showing signs of stress about the future of interest rates.

As the chart on page 1 shows, US government bond yields remain consistent with a long term downtrend despite the recent move higher. Nonetheless, movements in yields are also consistent with a change in direction, imposing a period of uncertainty on markets until a new direction has been more clearly defined.

While the latest market reaction was catalysed by the US labour market report, the charts of German and US yields show that the evolving changes in expectations go beyond domestic US conditions.

The US dollar remained on its recently declining trend although the trade weighted index is significantly higher than the mid-2014 value which prevailed prior to the most recent cyclical rise.

A falling US dollar is consistent with optimism about the outlook for global economic growth. While the recently legislated US tax cuts will support stronger US economic growth than might have otherwise occurred, the currency direction will depend to a large extent on expectations of relative performance which are less clear presently with Europe and Japan producing better than expected economic outcomes.

The Australia dollar remains in an uptrend but a reappraisal of US interest rate rises will be a drag on the Australian currency.

With interest rates not having been reduced as dramatically in Australia as in the USA and Europe, the scope to keep pace with rate rises elsewhere is limited. That could affect adversely the pace of ongoing Australian dollar appreciation.

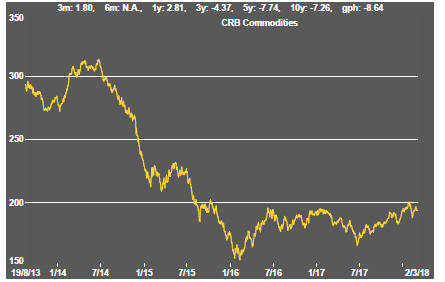

More favourable growth conditions and the weaker US dollar have helped support generally higher commodity prices.

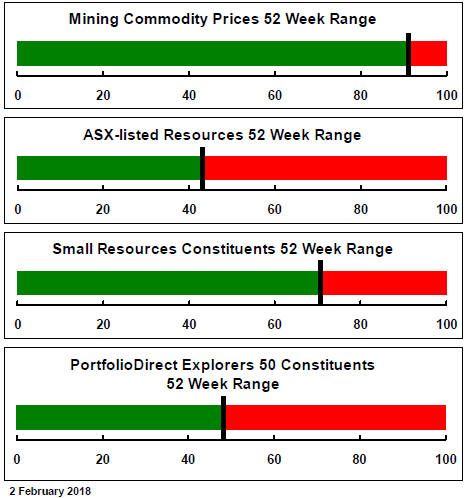

Nonferrous metal prices are sitting near the highest levels at the beginning of February than at any time since the beginning of 2017. Over 90% of the major mining commodity prices are at their 52 high prices.

Historically, mining related equity prices are more highly correlated with broader equity prices than they are to related commodity prices. This relationship was again evident the end of the week.

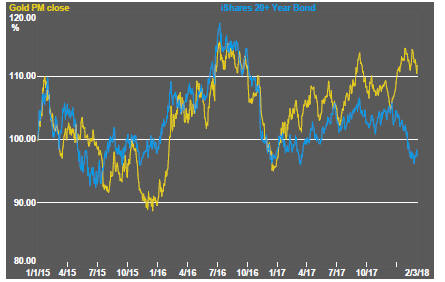

US gold related equity prices at the end of the week were affected adversely by the downward move in both gold prices and general equity market conditions.

The gold price faces a near term tug of war between the role of bullion as a safe haven during market turmoil and its role as a financial asset competing with rising yields on government bonds.

Rising bond yields would normally be associated with higher growth and accompanying expectations about rising inflation. The same conditions would normally support higher raw material prices and, in particular, higher copper prices which are more sensitive than other commodities to such conditions.

Copper prices are near their highest prices over the past four years but appear less leveraged than they have been historically to the combination of rising bond yields and a falling US dollar.

Recent rises in crude oil prices were not enough to retain gains for related exploration and production company equity prices as stock prices fell.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.