The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

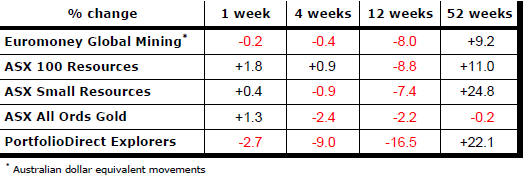

Resource Sector Weekly Returns

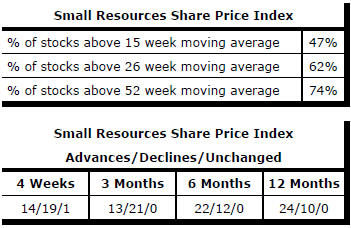

Market Breadth Statistics

Equity Markets

Talk of a global trade war and its potential impact on growth continued to roil markets.

The Chinese side continued to push back against steps by the US administration to punish the country for the trade imbalance.

Confusion among US administration spokespeople about the intentions of he president did not help ease the market tensions. Newly appointed chief economic adviser Larry Kudlow, trade adviser Peter Navarro and Treasury secretary Mnuchin all weighed in on whether the proposed tariffs were a step toward negotiations or intended to apply.

Their nuanced and sometimes inconsistent arguments about trade left market vulnerable to the Chinese threats to stand their ground.

Many hoped for the President himself, as the chief proponent of the trade measures, to move more aggressive to explain his intentions.

Whatever happens, any changes to tariffs will take several months to implement leaving the markets in a tug of war between speculations on trade policy and the outlook for earnings which are expected to grow by as much as 20% this year.

Added to the trade questions, Syria re-entered the frame after another chemical weapon attack on the local population. With Russia taking a more aggressive stance against western governments, a similar punitive attack to that conducted by the US and its allies a year ago, when Russia was given advance notice, appears to carry far greater risks.

Overall, option investors were pricing in higher share price volatility. Within the S&P500, divergences in sector performance persisted with sectors benefitting from lower yields performing more strongly than the financial services stocks.

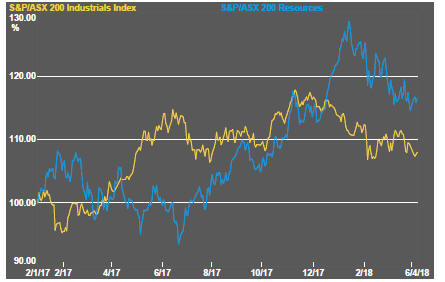

The mining sector has been more leveraged to worries about growth arising from a potential trade clash between the USA and China. Industrial sector leaders in the Australian market have continued to outperform resource sector stocks which continued to trend lower in Australia and gloabbally.

Interest Rates

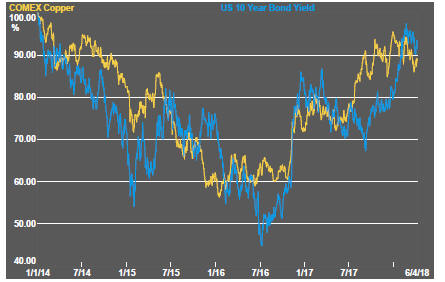

The rise in bond yields has halted as optimism about global growth conditions have appeared to ebb.

Despite stated beliefs by policymakers about rising inflation, demand for government securities remain strong.

The quality of European corporate debt is making government debt more attractive to hold.

Federal Reserve chairman Powell spoke during the week about monetary policy with investors especially interested in whether ructions over trade might have an influence on the stance of the Fed.

Powell did not foreshadow any change in the path of policy previously released and indicated that the Fed was not contemplating a response to the trade policy changes in part because they were too ill-defined to affect judgments.

Employment grew at a slower pace than it had in recent months, according to the monthly employment report for March with nothing in the wages outcome to detract from a view of relatively gentle upward pressure on infaltion.

Exchange Rates

The downward directional shift in the US dollar has stalled amidst competing views about relative growth rates, fears about disruption to trade patterns and the funding requirement of the US government. Some downward pressure in the past week left the currency within the bounds of where it has been for the last several weeks.

The newly legislated tax cuts and an omnibus spending bill tailored to get enough votes in both houses of the US Congress suggest longer term downside consistent with a history of a weakening currency occasionally punctuated by unsustained cyclical rises (see page 1).

The gentle upward drift in the Australian dollar could remain intact as long as risks to global economic conditions remain lowered and commodity prices are in the upper end of the range of prices in the past year.

Within that trend, tightening monetary conditions in the USA and, later, in Europe could exert more downward pressure as they occur contributing to within-trend fluctuations.

In the near term, trade disputes between the USA and its major trading partners in Canada, Mexico, Europe, Japan and China could add headwinds for any country potentially caught in the crossfire, including Australia.

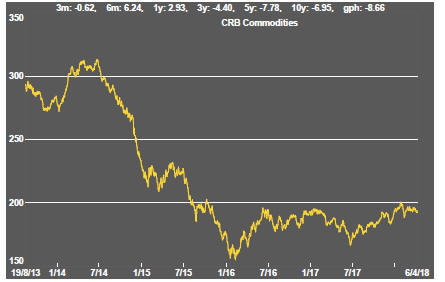

Commodity Prices

The general upswing in commodity prices over the past year remains within the bounds of a cyclical trough suggesting still stronger economic activity will be needed to carry prices higher.

Gold & Precious Metals

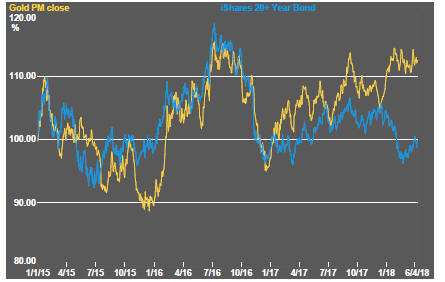

The gold price has been subjected to a tug of war between the negative effect of higher bond yields and the positive influence of a weaker US dollar. Overlaying those macro factors more recently has been anxiety about the rising trade rivalry between the USA and Europe and China.

The net result of the various factors driving prices had been a sharp rise in gold bullion prices resulting in a break in the link with bond prices.

Prices of Australian gold related stocks have moved within a narrower range than their north American counterparts. Australian prices still sit toward the upper end of the range of outcomes over the past year. In contrast, North American prices are around the lower end of their range.

Both groups of stocks have shown less than historical leverage to higher bullion prices. The North American stocks have shown the stronger connection to financial market conditions over the past month.

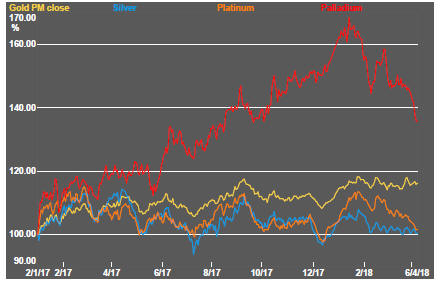

Within the precious metal complex, palladium and platinum prices were notably lower.

Nonferrous Metals

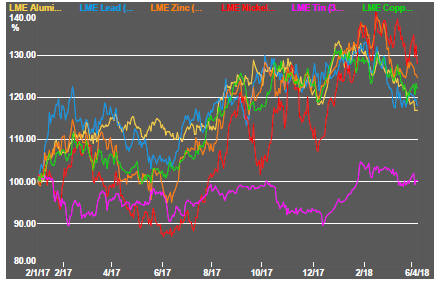

Prices of the main daily traded nonferrous metals had become increasingly correlated as a broadening consensus about the lowered risks to world economic activity emerged.

Tin prices have lagged conspicuously over the past year but showed a similar rise to that of other metals (and a lesser subsequent decline) since late in 2017.

All prices have tended lower as concern about disrupted international trade patterns have intensified and as (still minor and ambiguous) signs of weakness in Chinese activity rates have had an effect.

Bulk Commodities

Bulk commodity prices continued their move lower as sign of lowered Chines momentum after the first quarter began to show..

Increased Chinese steel production in the first quarter of 2018 has resulted in larger inventories. The inventory climb and threat of tariffs affecting Chinese steel demand have dragged steel prices lower and raised risks for metallurgical coal markets.

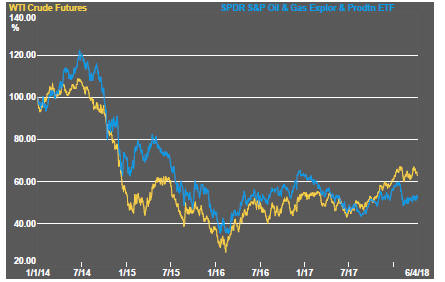

Oil and Gas

In a similar reaction to that evident among the gold stocks, US equity prices for oil and gas explorers have been dominated by broader stock market movements rather than movements in the price of crude oil.

Risisng US production, partly in response to higher prices, remains a burden on investor expectations about the likelihood of further oil price rises with continuing rises in oil rig productivity supporting higher output.

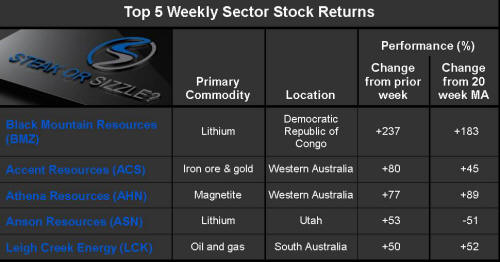

Battery Metals

Eighteen months of rising lithium-related stock prices has given way to a period of market reassessment as a lengthy pipeline of potential new projects raises the prospect of ongoing supplies being adequate for expected needs.

Potential lithium producers have been able to respond far more quickly to the various market signals than has been the case in other segments of the mining industry.

Battery metals remain a focal point for investors with recent attention moving to cobalt and vanadium.

Uncertainty over how a peaceful transfer of power can occur in the Democratic Republic of the Congo has added a dimension to cobalt prices lacking in other metals caught up in the excitement over transport electrification.

Uranium

The uranium sector is once again moving along the bottom of its long term trading range in the absence of more meaningful signs that power utilities are prepared to re-enter the contract market to negotiate their longer term needs.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.