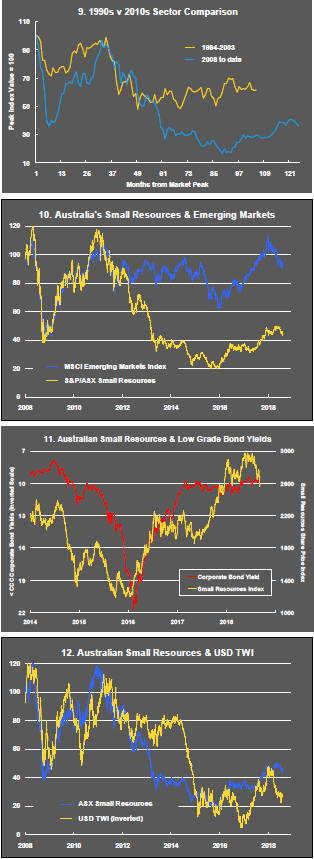

The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

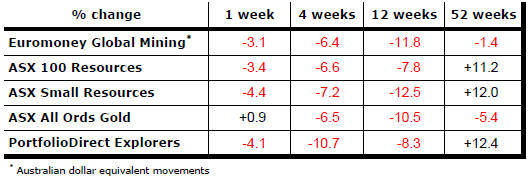

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

Resource Sector Weekly Returns

Market Breadth Statistics

52 Week Price Ranges

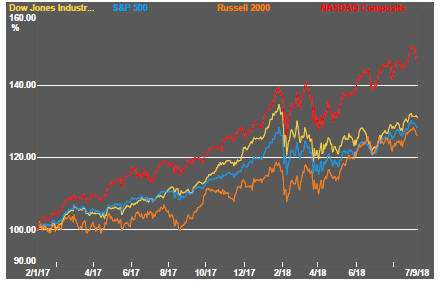

Equity Markets

Weaker equity prices were driven by an increasingly familiar mix of trade policy tensions, developing economy risks, slowing global growth, currency ructions and changing expectations about monetary policy settings.

Prices of information technology stocks in the US weakened as concerns about the business models of social media sites became more prevalent but all significant sectors have been losing momentum.

Another week passed without resolution of trade disputes with the USA. President Trump added Japan to his list of trade targets as discussions commenced with that country’s representatives. Canadian negotiators once again expressed optimism about reaching agreement on a revised NAFTA without being able to close the gap with their US counterparts.

Labour market statistics released by the US government at the end of the week showed an employment gain in August ahead of what economists had expected and a wages growth acceleration. The labour market data seemed to confirm that another interest rate rise would be initiated by the Federal Reserve later in September.

The debate about future policy is becoming more influential in dictating the direction of equity prices as differences of opinion emerge about whether the Federal Reserve will move more or less quickly than currently anticipated in response to changes in economic conditions.

Resource Sector Equities

Mining sector equities, which had already been in a downswing, were dragged still lower by the more generalised equity market weakness.

The fall in Australian mining equities will have been cushioned by a weaker Australian dollar.

Global mining sector prices fell by more than 3% during the week to take the index below its level from 52 weeks ago. The gap in performance between the market leaders and the exploration end of the sector narrowed during the week after the largest stocks had been outperforming the small stocks over the past three months.

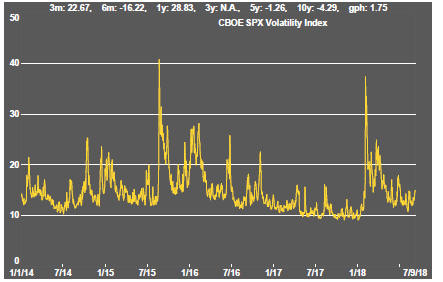

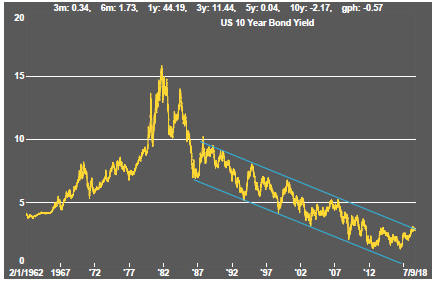

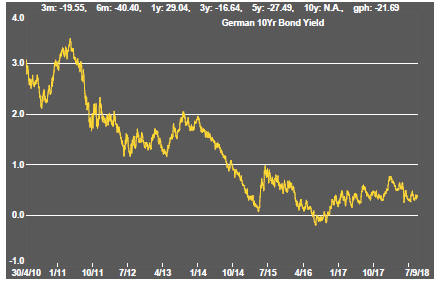

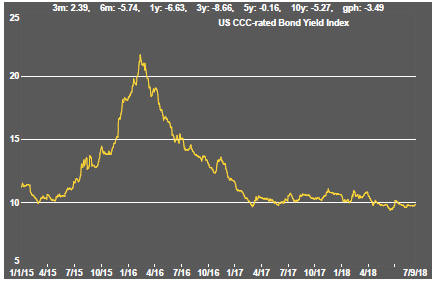

Interest Rates

US Bond yields rose following the release of unexpectedly strong August labour market statistics on Friday although 10 year yields have remained below 3%. US dollar denominated corporate debt price indicators remained firm.

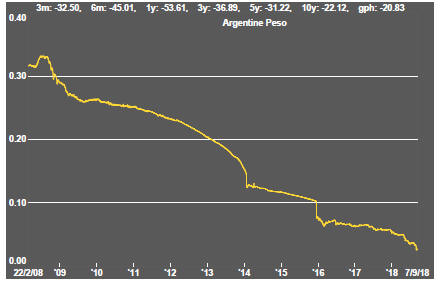

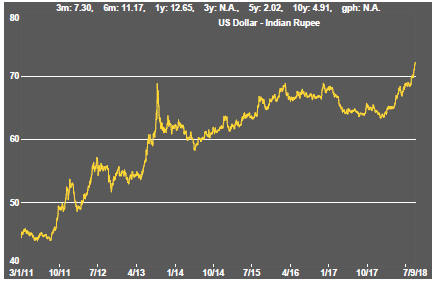

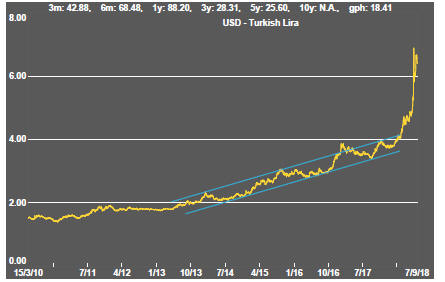

Developing country central Banks were opting for more aggressive steps to stall falling currencies. Argentina moved to help finalise an agreement with the International Monetary Fund and Turkey appeared set to also move despite the Erdogan government having previously expressed strong opposition to hiking interest rates to avert capital outflows.

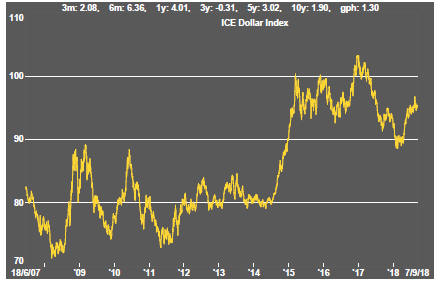

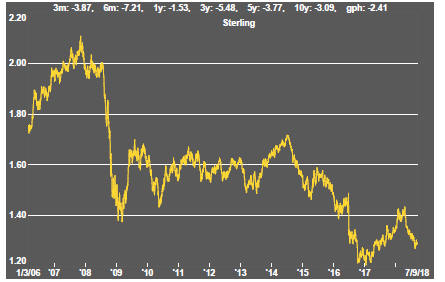

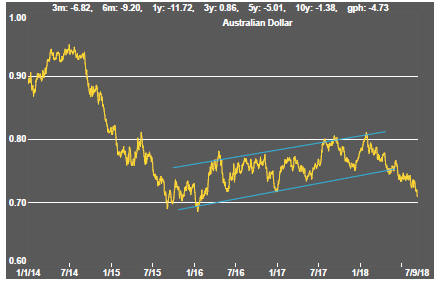

Exchange Rates

The US dollar edged higher as a wide range of other currencies declined. Sterling remained hostage to news about Brexit. The European negotiators, at one point, talked more optimistically about reaching an agreement, helping the currency, but British prime minister Theresa May has been under growing pressure from members of her own party to abandon her plans in favour of a cleaner break with Europe, adding to the downward pressure.

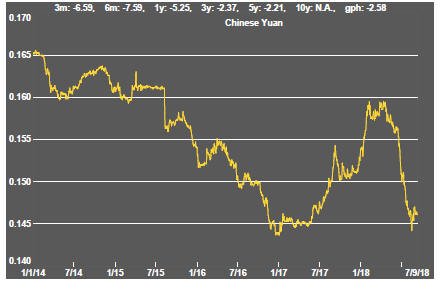

While there were signs of some easing in the rate of developing country currency declines, the Australian dollar gave up more ground as concerns about Asian regional growth took its toll.

Commodity Prices

The general upswing in commodity prices since mid 2017 had been given added impetus by stronger crude oil prices.

Diminished momentum has left prices within the bounds of a cyclical trough, albeit at the upper end.

The flip side of the benefits for commodity producers and exporters of higher commodity prices is the cost pressure now being experienced by users of agricultural and raw material commodities. Reporting companies have been suggesting this as a source of margin compression.

Business surveys closely watched by central banks are showing signs of upward pressure on selling prices as a result of higher raw material prices.

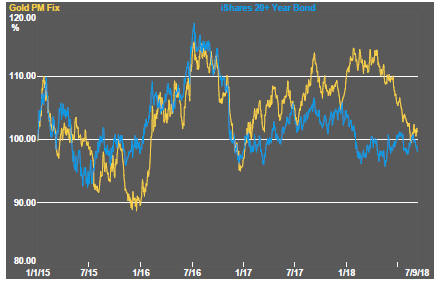

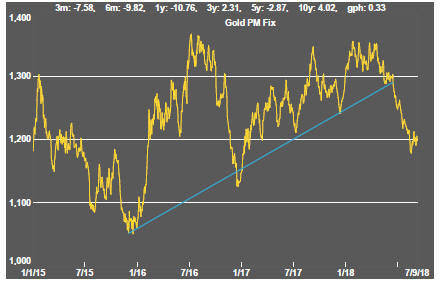

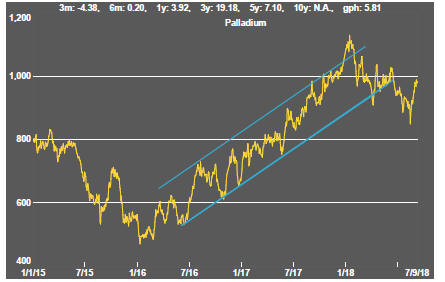

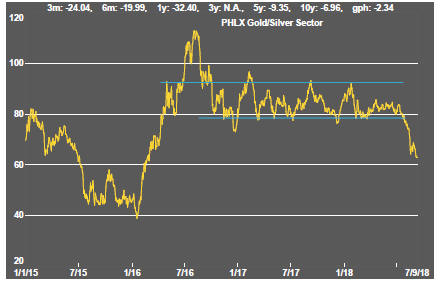

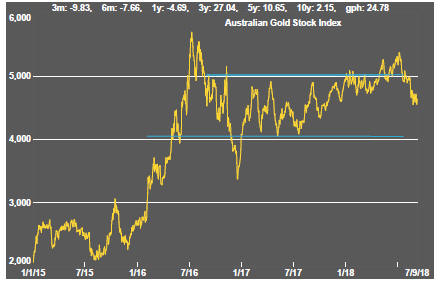

Gold & Precious Metals

Gold prices stabilised despite the tendency to higher interest rates as demand for US dollar denominated assets generally remained strong.

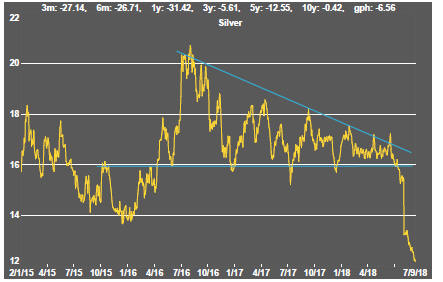

While the palladium and platinum price decline stalled, silver prices continued their sharp descent.

The precious metal price movements were echoed in the movements of related equity prices although the potential fall in Australian gold sector prices has been cushioned by the weakening Australian dollar.

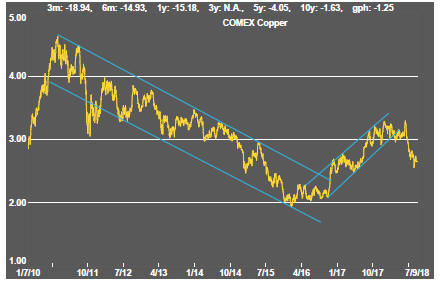

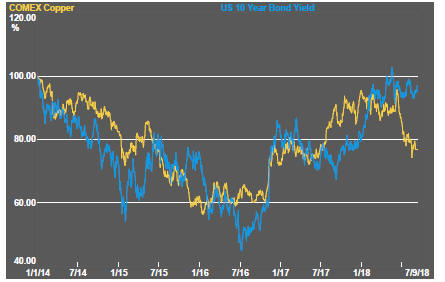

Nonferrous Metals

All of the major daily traded non-ferrous metal prices were heading in the same direction as they appear to have set out on a new cyclical path since February.

Slightly higher bond yields which would normally suggest improved growth conditions favouring higher raw material prices have not been reflected in the metal price movements which suggest weakening global growth conditions.

Metal prices are less US-centric than bond yields and, consequently, a more telling indicator of what is happening to the global economy overall.

Perhaps US bond prices would have been lower had non-US economic outcomes matched those in the world’s largest economy.

The apparent tension between US bond yields, on the one hand, and metal prices, on the other, is something to watch as a guidepost to the balance of influences in a desynchronised global economy.

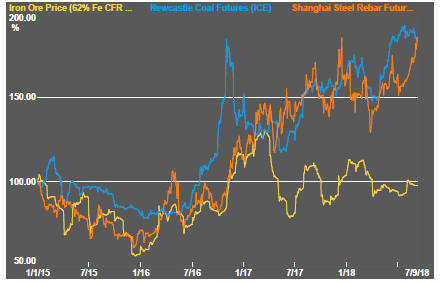

Bulk Commodities

Chinese economic growth reports show the national economy meeting its targets, as one would expect for a centrally planned economy, but appears to be only doing just enough. There are no signs of upside risk. The tariff fight with the USA is beginning to take a toll on activity rates in an economy with a bias toward less strong growth in the years ahead, in any event.

Higher steel prices have not been reflected in stronger iron ore price outcomes. Coal prices continue at high levels reflecting China’s drive to source cleaner energy and as constraints on new mine development keep a rein on supplies.

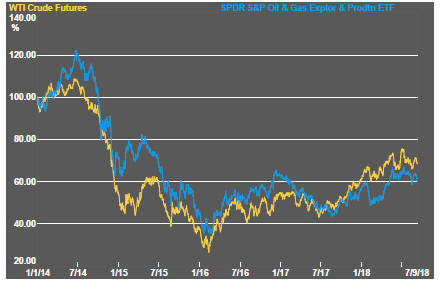

Oil and Gas

The upward trend in crude oil prices has given way to a leveling out in price with another fall in the past week.

OPEC production decisions have helped to support prices as has reimposition of economic sanctions by the US government on Iran. The failure of effective government in Venezuela has been another contributing influence.

The Iranians have been lobbying European countries to prevent more widespread application of sanctions but the likelihood of relief appears slim as long as funds must circulate through US banks.

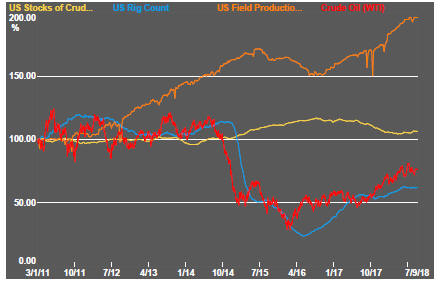

US production, in any event, continues to rise and is now matching output from Russia and Saudi Arabia. Texas alone is positioned to be the third largest producer after Russia and Saudi Arabia.

Despite the change in tone within crude oil markets, related equity prices have been muted in their responses, implicitly signaling scepticsm about the sustainability of price rises when they have occurred.

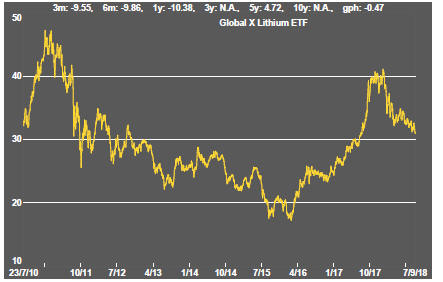

Battery Metals

Eighteen months of rising lithium-related stock prices have given way to a prolonged period of market reassessment as a lengthy pipeline of potential new projects has raised the prospect of ongoing supplies better matching expected needs.

Potential lithium producers have been able to respond far more quickly to market signals than has been the case in other segments of the mining industry where development prospects have been slowed by reticence among financiers to back development.

Movements in lithium related equity prices had been aligned more closely with overall sector equity prices in recent weeks.

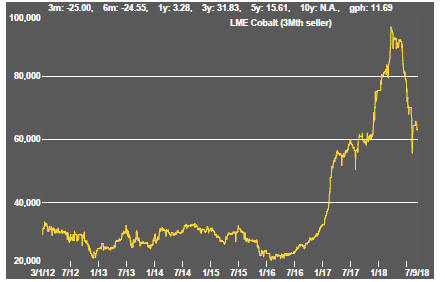

Battery metals remain a focal point for investors with recent attention moving to cobalt and vanadium.

Doubts about a peaceful transfer of political power in the Democratic Republic of the Congo (and instances of Ebola) have added a dimension to cobalt prices lacking in other metals caught up in the excitement over the longer term impact of transport electrification.

In the longer term, cobalt is the most vulnerable of the battery related metals to substitution with high prices likely to stimulate research in that direction.

A spokesperson for Panasonic, manufacturer of batteries for Tesla motor vehicles, has been quoted as saying that the company intends to halve the cobalt content of its batteries because of uncertainties over supply.

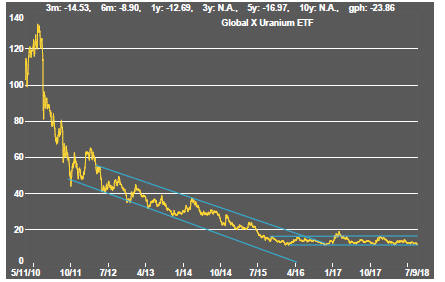

Uranium

The uranium sector is in the midst of forming a prolonged cyclical trough as market balances slowly improve. Power utilities are still not prepared to re-enter the market for contracted amounts of metal to meet longer term needs. A slight upward bias in prices has been evident in the past month.

Slightly higher equity prices from time to time, in the hope of improved conditions, have not been sustained but could be repeated as speculation about improved future demand ebbs and flows. The effect of an announcement by Canadian producer Cameco to extend the duration of its previously implemented production cut gave the market a very slight but quickly lost lift.

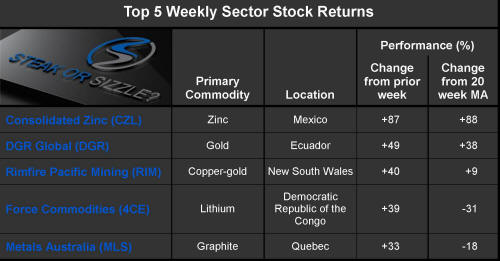

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.