The Big Picture

After recovering through 2010, a lengthy downtrend in sector prices between 2011 and 2015 gave way to a relatively stable trajectory similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of frequent macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability in sector prices suggests a chance for individual companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low some 90 months after the cyclical peak in sector equity prices but these conditions were reversed through 2016 and 2017 although, for the most part, sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

In the absence of a market force equivalent to the industrialisation of China, which precipitated an upward break in prices in the early 2000s, a moderate upward drift in sector equity prices over the medium term is likely to persist.

The Past Week

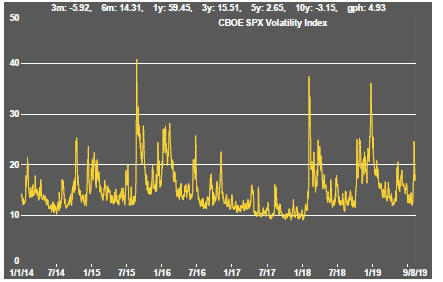

Unusually strong intraday swings modified the net change in equity prices but a swift sentiment switch during the week left markets reeling.

Moves in prices of equities, bonds, foreign exchange and commodities marked the week.

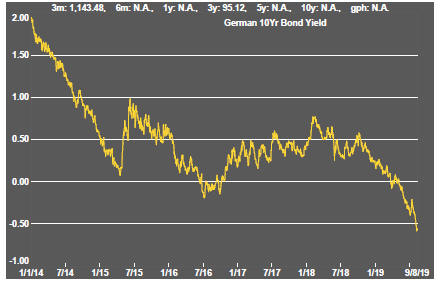

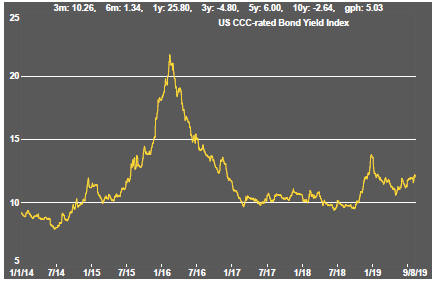

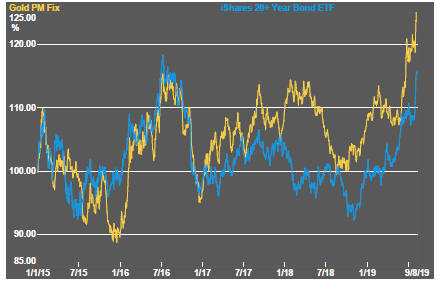

The downward bias in global bond yields leaves the Fed Funds rate at risk of being a conspicuous outlier in the global interest rate structure.

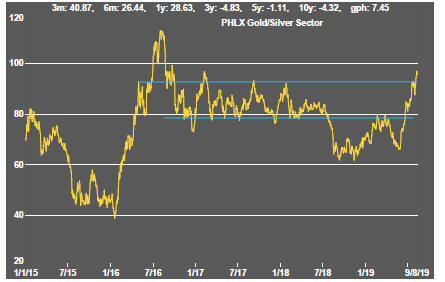

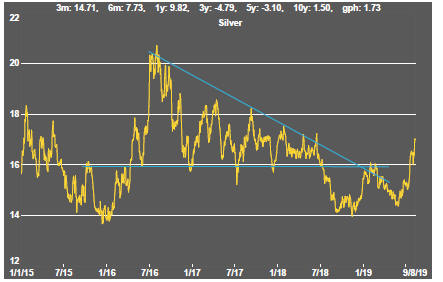

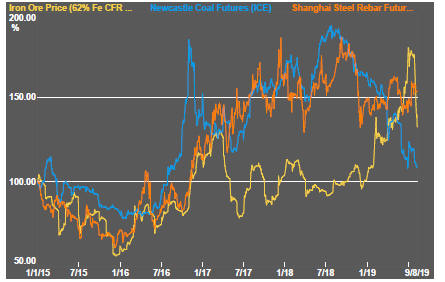

Among commodities, gold prices touched US$1,500/oz for the first time since 2013. The iron ore price has lost 25% over the past month after recent supply constraints and strong Chinese steel production had driven prices higher.

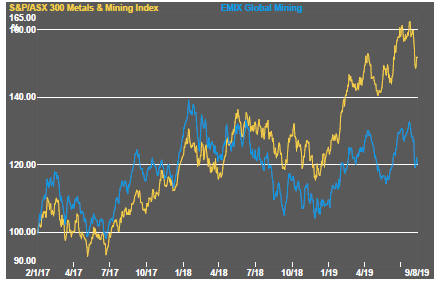

Resource sector equity indices, consistent with the commodity price moves, were led lower by the iron ore exposed market leaders while gold stocks rose. The small end of the market - mostly exploration companies - posted gains.

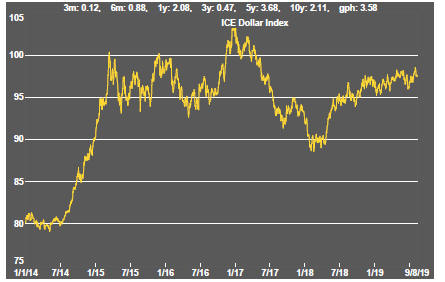

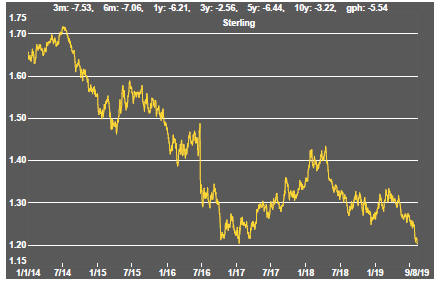

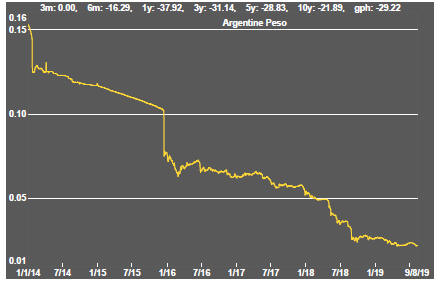

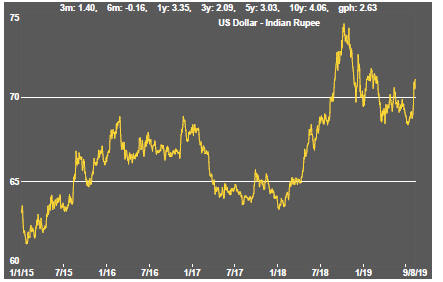

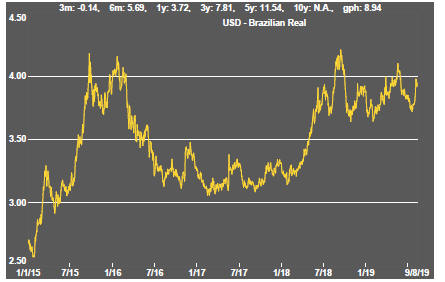

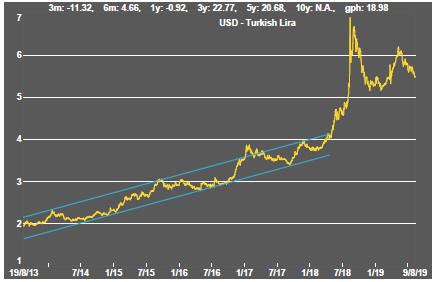

Within foreign exchange markets, a lower Australian dollar lifted ASX-listed miners. Devaluation of the yuan raised the prospect of currencies being weaponised in the US-China trade conflict. Continued weakness in sterling reflected an apparent breakdown in EU-UK communications in the aftermath of threats by the newly formed Johnson administration to unilaterally withdraw from the European Union at the end of October.

Daily traded non-ferrous metal prices remained surprisingly steady overall against the backdrop of large swings in the prices of a wide range of financial assets. The nickel price has returned to the cyclcially high levels of early 2018. The prices of the other principal metals are below their early 2018 levels with the zinc price touching its lowest point since then. The tin price has fallen 20%.

The disparity between copper price and bond yield moves has extended further, reinforcing the prospect of a future resolution of the performance disparity. One or other of the bond or copper market appears to have a mistaken view about the prospects for global growth.

The crude oil price finished the week edging lower but overall remained little changed after Saudi Arabian officials discussed the possibility of making short term cuts to production ahead of more formal scheduled production decisions involving OPEC and Russia.

European economic weakness was highlighted by the release of especially weak industrial production data for Germany and a contraction in UK GDP in the second quarter of 2019.

Italy faced the prospect of fresh elections after one of the parties in the currently governing coalition threatened withdrawal of its support, aggravating the inability of Europe to grapple with a nasty combination of systemic and cyclical problems.

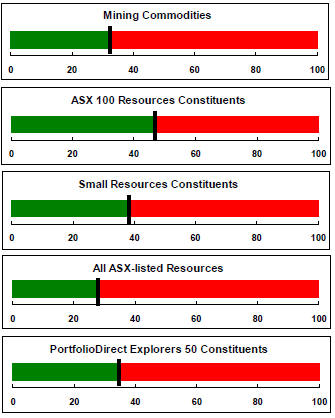

Sector Price Outcomes

52 Week Price Ranges

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.

Equity Market Conditions

Resource Sector Equities

Interest Rates

Exchange Rates

Commodity Prices Trends

Gold & Precious Metals

Nonferrous Metals

Bulk Commodities

Oil and Gas

Battery Metals

Uranium