The Big Picture

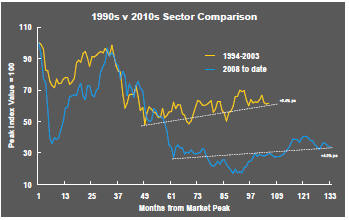

After recovering through 2010, a lengthy downtrend in sector prices between 2011 and 2015 gave way to a relatively stable trajectory similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of frequent macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability in sector prices suggests a chance for individual companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low some 90 months after the cyclical peak in sector equity prices but these conditions were reversed through 2016 and 2017 although, for the most part, sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

In the absence of a market force equivalent to the industrialisation of China, which precipitated an upward break in prices in the early 2000s, a moderate upward drift in sector equity prices over the medium term is likely to persist.

The Past Week

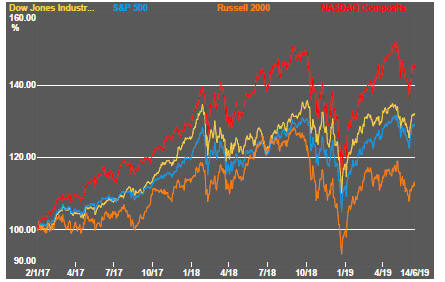

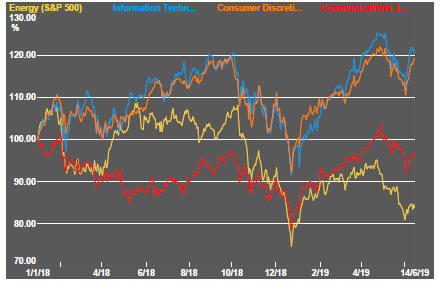

Equity prices pushed higher as central bankers around the world re-emphasised their commitments to support economic activity and boost inflation.

Financial markets have embraced the now widely held lower growth prognosis. Markets appear to be bullying the major central banks into changing their policies. This is most apparent in the USA where the Federal Reserve has turned with unusual speed from a rising interest rate path to one more in line with what markets wanted to hear.

The change in expressed Fed attitude has occurred even as the chairman has been putting the case for the economy being in a good place. Strangely, at the same time, the US administration is arguing that the economy remains strong even as it demands that rates it should be cut and President Trump talks threateningly about removing Fed chairman Jerome Powell from the job for delaying action to reduce rates.

Uncertainties over trade policies have continued to plague business investment decisions. While the US consumer appears to remain in robust good health, business investment is weak and the contribution to growth from exports is uncertain. US manufacturers are reporting deteriorating new export order flows. Flagging investment and weak export orders pose a rising risk for employment and income growth.

President Trump’s reference to a phone call with Chinese president Xi buoyed equity markets which are now highly leveraged to the outcome of discussions between the two at the upcoming G20 leaders’ meeting in Japan later this month.

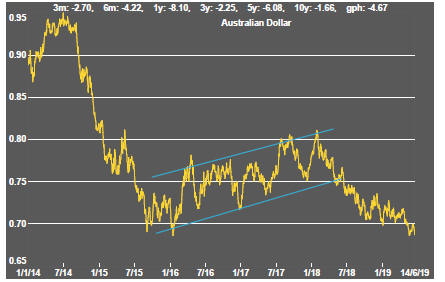

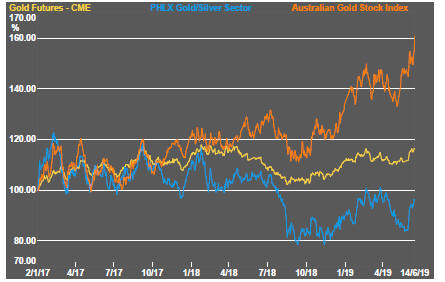

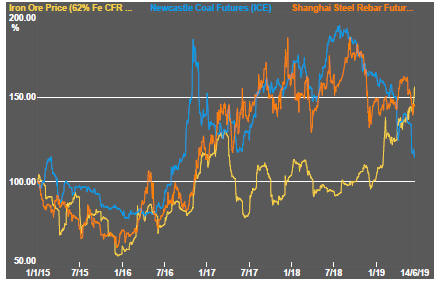

Stronger equity market conditions were reflected in the headline mining share price indicators. Added benefits came from further rises in iron ore prices favouring the sector leaders and, for Australian listed companies, further weakness in the Australian dollar.

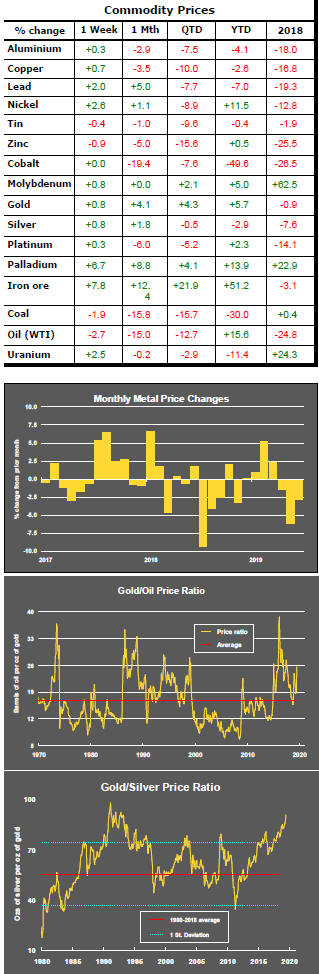

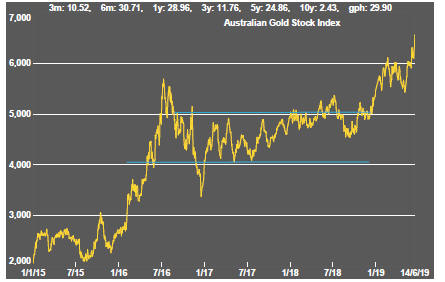

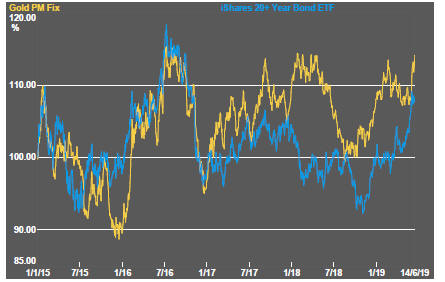

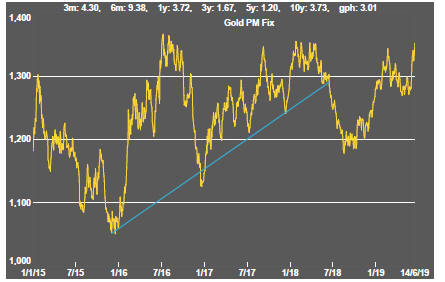

The ASX listed gold segment has benefited from higher gold prices as well as the weaker currency. The rise in the gold price keeps it within the range of prices over the past three years but consistent with the repricing of financial assets globally as a result of the reappraisal of the growth Outlook.

Consistent with the rise in gold prices, silver prices also rose but continued to lag gold prices pushing the prices of the two metals toward a historically large disparity.

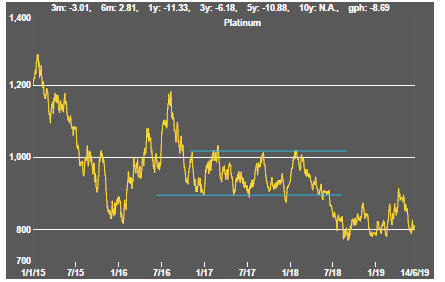

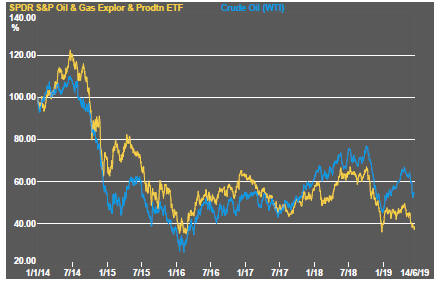

Daily traded nonferrous metal prices remain consistent with threats to global growth as does the crude oil price which is pushing lower as analysts reappraise the near-term demand outlook, even as geopolitical pressures on supply intensify. US crude supplies have continued to rise.

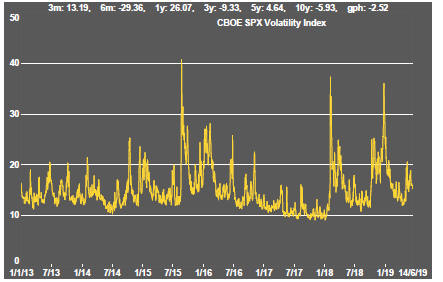

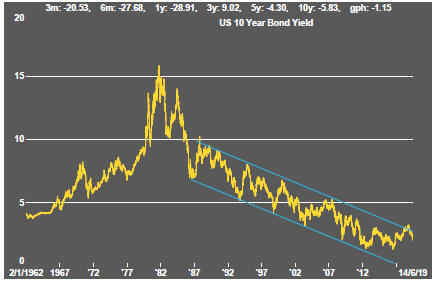

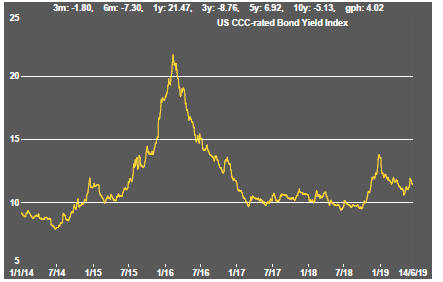

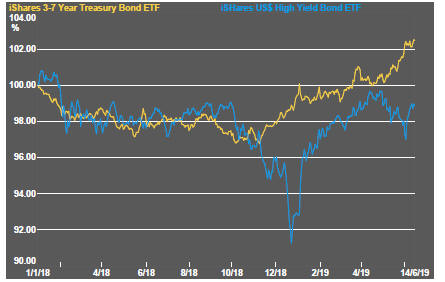

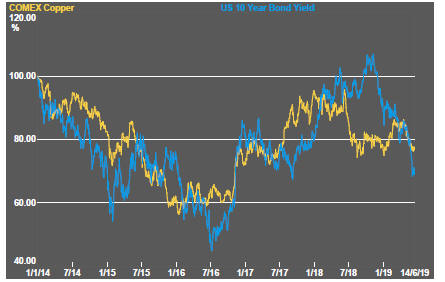

The spread between government debt yields and yields on high risk corporate debt has widened signalling tougher financing conditions for miners with development projects.

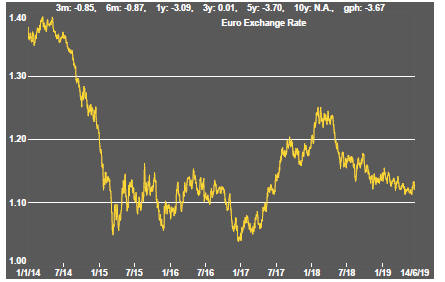

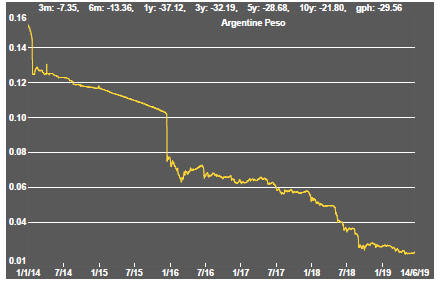

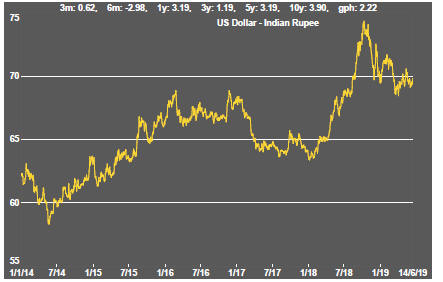

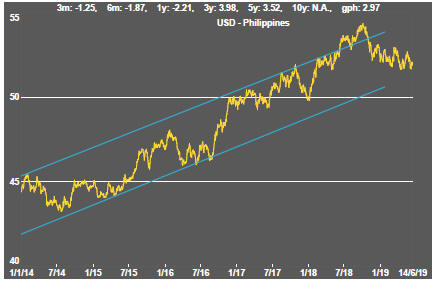

Exchange rate moves have been relatively modest in the context of such large or potentially significant global economic pressures. An exception has been the Australian dollar which is coming under pressure from a slowing domestic economy and after the Reserve Bank very explicitly foreshadowed a lowering of policy interest rates.

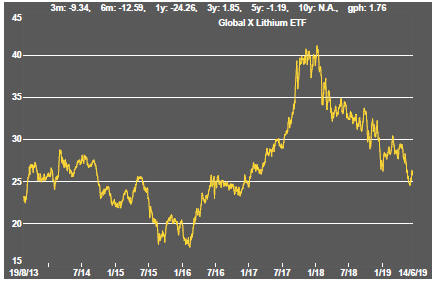

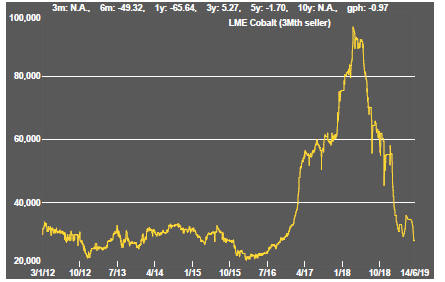

The battery metals complex which had created so much excitement is well off the boil with cobalt prices having given up all the gains from 2017-2018 and lithium equity prices under-performing broader mining sector price indices. Uranium prices have also lost momentum.

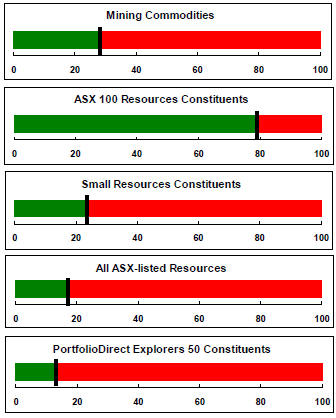

Sector Price Outcomes

52 Week Price Ranges

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.

Equity Market Conditions

Resource Sector Equities

Interest Rates

Exchange Rates

Commodity Prices Trends

Gold & Precious Metals

Nonferrous Metals

Bulk Commodities

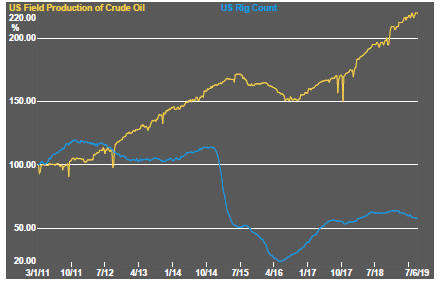

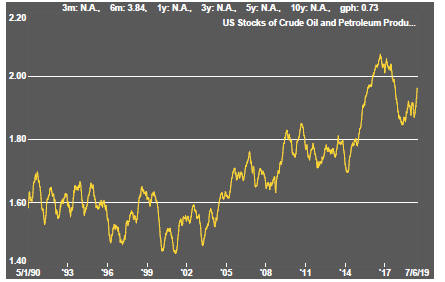

Oil and Gas

Battery Metals

Uranium