The Big Picture

After recovering through 2010, a lengthy downtrend in sector prices between 2011 and 2015 gave way to a relatively stable trajectory similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of frequent macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability in sector prices suggests a chance for individual companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low some 90 months after the cyclical peak in sector equity prices but these conditions were reversed through 2016 and 2017 although, for the most part, sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

In the absence of a market force equivalent to the industrialisation of China, which precipitated an upward break in prices in the early 2000s, a moderate upward drift in sector equity prices over the medium term is likely to persist.

The Past Week

Equity markets finished the week with an upward bias despite ongoing concerns about slowing global economic growth.

Evidence mounted that US growth had slowed significantly although labour market indicators, including an increase in job vacancies, continued to show firm conditions. Retail sales grew slightly after a sharp decline in December but manufacturing output fell for the second consecutive month and industrial capacity utilisation declined. The Atlanta Federal Reserve Bank is now forecasting an annualised first quarter GDP increase of just 0.4%, based on the flow of partial economic indicators.

The Chinese premier made a strong statement about his government’s determination to support activity. Further support limited deteriorating expectations about the country’s economic performance while, at the same time, conceding that growth would have been subsiding more quickly without concerted action.

Markets are looking ahead to what the US Federal Reserve governors say about the course of interest rates over the balance of 2019 following their upcoming meeting this week. The Fed is now an even more critical market ingredient after its dramatic January pivot away from further tightening.

Markets are being guided to expect a US-China trade deal despite a foreshadowed Trump-Xi summit being postponed until the details of an agreement have been fully hammered out. President Trump said that he will know in three or four weeks whether something can be achieved.

Risks associated with Brexit appeared to ease when the UK House of Commons voted against leaving the European Union unilaterally at the end of March. The vote - only advisory - possibly removed the withdrawal option most disliked by legislators but left unclear how the continuing impasse would be resolved.

A stronger sterling exchange rate, emanating from the decision to block a no-deal Brexit, contributed to a reduction in the upward pressure on the US dollar.

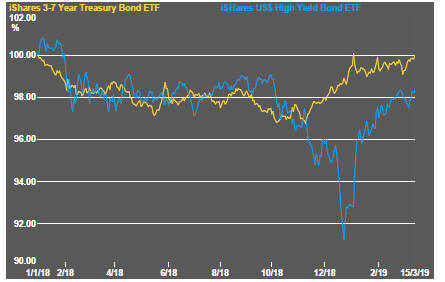

Financial market conditions continued to move in favour of higher risk corporate financing. This, the weaker US dollar and firm metal prices contributed favourably to resource sector equity prices which generally held their ground despite widening expectations of a slowdown in global economic activity.

Metal prices appear to be defying the changed view of global growth - and the interpretation of the outlook evident in financial markets - raising the risk of a subsequent realignment of interpretations. There is now possibly too much weight being placed on a favourable US-China trade deal within metal markets and insufficient attention being given to the preferred outlook within financial markets.

The gold price has failed to make headway against earlier price peaks in 2018 and 2016 suggesting it might have already run too far ahead of changed financial market conditions which had favoured some limited bullion price appreciation.

Resource sector equities continue to display limited leverage to improvements in commodity prices, where they occur. The clearest example of the lack of responsiveness has been in the oil market where the prices of exploration and production companies have suggested little confidence in the higher oil price being sustainable.

Sector Price Outcomes

52 Week Price Ranges

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.

Equity Market Conditions

Resource Sector Equities

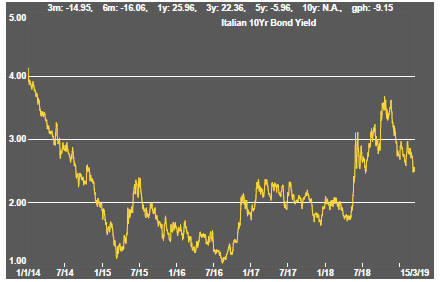

Interest Rates

Exchange Rates

Commodity Prices Trends

Gold & Precious Metals

Nonferrous Metals

Bulk Commodities

Oil and Gas

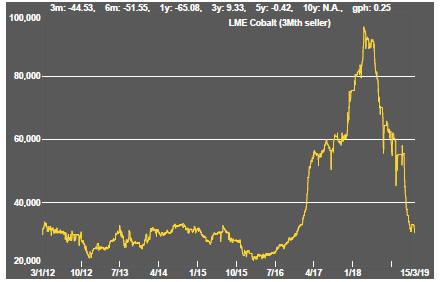

Battery Metals

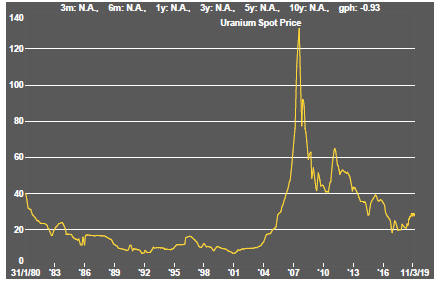

Uranium