The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

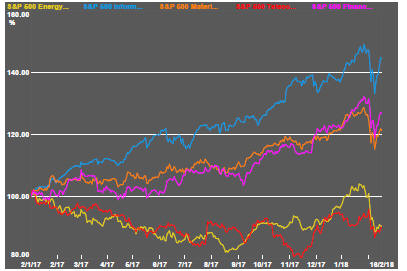

Resource Sector Weekly Returns

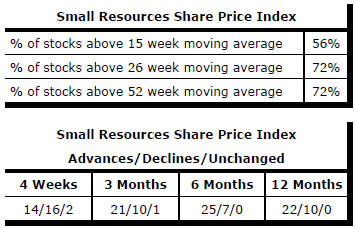

Market Breadth Statistics

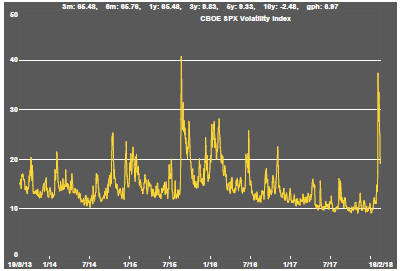

Markets bounced back with surprising strength as measures of volatility declined and investors seemed to put aside concerns about inflation, which had loomed large after the January US labour market report.

Lowered risks to global growth and confidence about corporate earnings appear to have overridden fears that interest rates will be driven higher more quickly than had been expected.

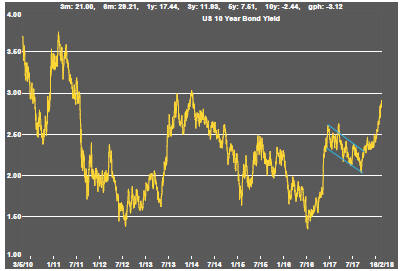

Financial markets have led the reappraisal of market conditions with a relatively dramatic rise in US government bond yields anticipating a large prospective change in monetary policy settings.

Although the rise is cyclically strong, the current position (under 3% on 10 year bonds)remains within the range of what investors would have considered "normal" based on targeted policies before the recent rise had commenced.

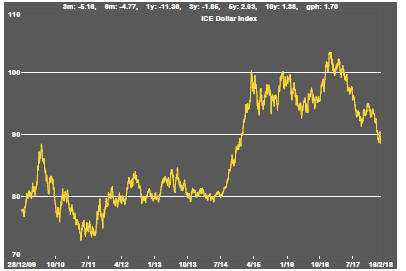

Exchange rate moves remain an important influence on markets.

The decline in the US dollar has abated somewhat in the past week as the crosscurrents affecting currency movements - including capital flows and relative interest rate movements - have become more ambiguous in their influence.

The Australian dollar which is critical to the underlying value of Australian miners remains in a broad upward trend despite interest rate movements acting against the Australian currency.

Markets would be, as usual, influenced by the direction of commodity prices which are generally regarded as an important influence on the Australian currency.

The gold price has been subjected to a tug of war between the negative effect of higher bond yields and the positive influence of a weaker US dollar. The net change in bullion prices has been relatively modest despite the sometimes unusually large swings in macro variables.

Within the precious metal segment, palladium prices have swung strongly in both directions after having been on a rising trend for over a year.

The forces which have contributed to higher bond yields would have normally had a positive effect on industrial raw material prices, especially for copper which has historically been sensitive to such factors. The copper price might have been an early warning of the rise in bond yields which followed shortly after the copper price life in the second half of 2017.

Prices of the main daily traded nonferrous metals have become increasingly closely correlated with a broadening consensus about the lowered risks to world economic activity.

Tin prices have lagged conspicuously over the past year but have showed a similar rise to that of other metals since late in 2017.

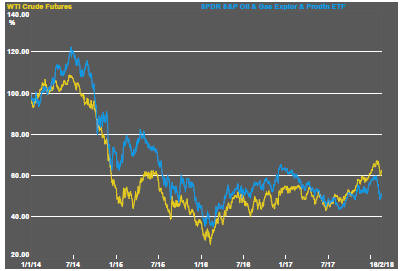

An easing in crude oil prices as US production expansions coincided with weaker financial markets has prompted a slightly more marked negative response among related exploration and production companies.

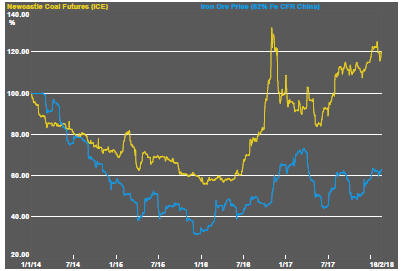

The bulk commodity response to the change in macro conditions has been stronger within the coal market than for iron ore. The coal market will have been a beneficiary of increasingly constrained supplies with capacity being closed in Asia and development plans elsewhere under threat.

Uranium prices which had shown some very slight upward movement in late 2017 have not been carried forward by cuts in production signaling that abundant supplies remain available.

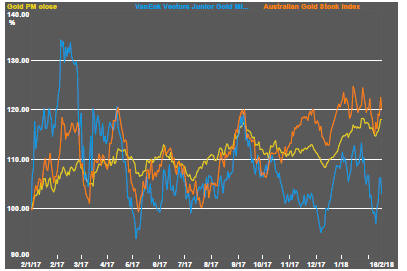

The related equity prices have lost momentum after strong bottom of the cycle gains following two of the world's largest producers announcing production cuts to help rebalance the market.

Uranium equity prices are again closing in on the lower end of a trading range extending back two years.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.