The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

Resource Sector Weekly Returns

Market Breadth Statistics

52 Week Price Ranges

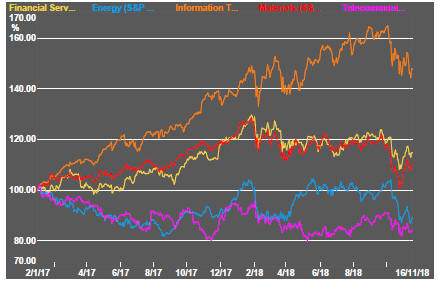

Equity Markets

Global equity markets remained highly volatile within each of the trading days but further falls over the course of the week were averted.

US-Sino trade tensions have been an important recent guidepost to movements in US markets. President Trump said, during the day week, that China wants a deal although officials walked back from the comments characterising them as the president wishing to remain optimistic rather than there being an imminent accommodation between the two countries.

At other times, US officials were critical of Chinese behaviour, inviting scepticism about whether any formal agreement, if one eventuates, will be anything more than a mechanism to deescalate the rhetoric.

That said, any agreement might be enough to buoy markets, at least temporarily, if the threat of further disruption to trade flows is removed.

Trade aside, US monetary policy appears likely to persist as an influence on the market for many months.

The Federal Reserve has tried to be as transparent in its view of how policy will evolve so as to maximise certainty for investors. Its attempts at transparency are now proving a double edged sword.

Rising asset values were a part of its plans to strengthen economic growth. Further into the cycle, financial markets are a less important mechanism for effecting employment and inflation goals.

With economic growth seemingly past its prime and corporate earnings growing less quickly, investors have become increasingly fearful that the Federal Reserve will damage market performance if it implements the policy implicit in its existing guidance.

Comments by Federal Reserve governors during the week about the direction of policy contributed to market volatility, including the large intraday movements.

Although volatility has remained elevated, losses have generally not been indiscriminate or suggestive of panic selling. The absence of panic selling could mean that further weakness is on the cards before a firm bottom, based on a reassessment of valuation and risk, is established.

Sector performance has suggested a swing away from growth-oriented momentum stocks which have typified the market drive higher.

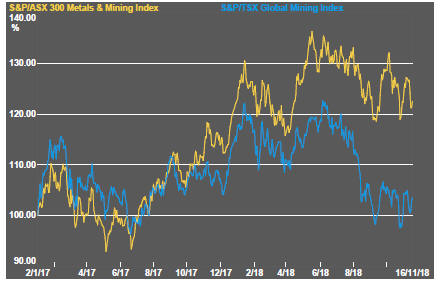

Resource Sector Equities

Volatility in the broader market has been reflected in the mining and oil and gas sectors with the energy sector being especially weakened by falling crude oil prices.

Lower oil prices have added to investor anxiety about global growth.

Resource sector equities have been affected adversely by the swing in investor sentiment although the impact has been moderated by the sector not having enjoyed an especially strong cyclical rise.

Within the week, the exploration stocks which had underperformed the leading stocks in the sector produced a net positive return.

Gold related equities generally held their ground with support from relatively firm bullion prices although the negative equity price influences were also evident in the market fluctuations.

Interest Rates

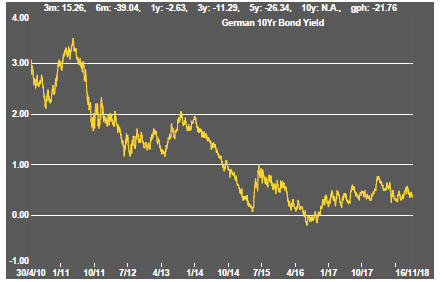

US government bond yields have retraced from their highest recent levels despite expectations of further interest rate rises. Fund flows away from riskier assets have helped sustain bond prices. Some modification to interest rate expectations has also helped.

Four further rate rises over the coming 12 months had been a widely held expectation in US financial markets until recently when economists started to more explicitly question the Fed’s intentions. Some now see recession forcing the Fed to backtrack. Although this is a minority view, the risk is sufficiently prevalent for the likelihood of all rises to have been pared back, according to surveys of forecasters.

Fed officials have added to the evolving reappraisal by questioning how certain they can be about the level of interest rates which can be characterised as “neutral”.

Comments from Fed Chairman Powell that “neutral” was a very long way off spooked markets by implying that a succession of rate rises would occur before the goal was reached. On the other hand, another Fed governor acknowledged that it was too hard to be precise, suggesting that policy makers will recognise neutral when they see it and, in the process, raising a big question about the meaningfulness of presenting quarterly projections of their policy intentions for the following two years.

The upward movement in low grade corporate bond yields has become more pronounced. While yields are well below the cyclically high levels reached in 2016, the trend is negative for miners looking for US dollar funds in capital markets.

Exchange Rates

Currencies seemed to suffer from the same influences contributing to equity and financial market volatility.

The upward bias to the US dollar has persisted with a negative effect on US corporate earnings. Deteriorating European growth prospects have weighed on the euro. Sterling has been pushed and pulled by news about progress toward a Brexit agreement and turmoil within the British Conservative Party precipitated by the content of the final agreement.

During the week, the UK government had appeared on the verge of collapse but was most likely saved by there being no alternative policy being on offer and having the support of a meaningful number of legislators to the one agreed by a majority of ministers.

Developing country currency pressures continued to ease with the Australian dollar appearing to be especially leveraged to an improvement in sentiment.

Commodity Prices

The general upswing in commodity prices since mid 2017 had been given added impetus by stronger crude oil prices.

Subsequently diminished momentum has left prices within the bounds of a cyclical trough, albeit at the upper end.

The flip side of the benefits for commodity producers and exporters of higher commodity prices is the cost pressure now being experienced by users of agricultural and raw material commodities. Reporting companies have been suggesting this as a source of margin compression.

Business surveys closely watched by central banks are showing signs of upward pressure on selling prices as a result of higher raw material prices.

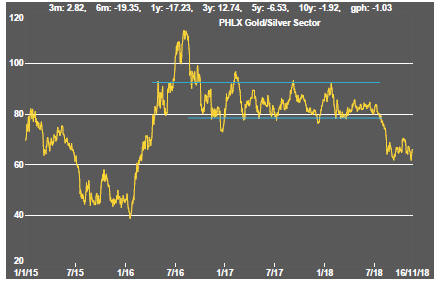

Gold & Precious Metals

Amidst sometimes wild gyrations in equity prices, gold bullion prices have changed a little.

The firmer US dollar and expectations of rising interest rates will have held back bullion buying. The recent decline in US government bond prices has not been reflected in gold bullion prices, leaving open the possibility of more significant adjustments even without further yield moves.

The disparate price performance among the various precious metals remains evident with silver prices to face the strongest headwinds.

Nonferrous Metals

The prices of the daily traded nonferrous metals showed divergent moves during the week and nothing which might reflect concerns about global economic growth (a 6% fall in crude oil prices being attributed to fears of slowing growth).

All the main London traded prices are now below the levels at which they started in 2018 with tin, for so long the laggard, now showing the best relative performance over the year to date.

The copper price has been at odds with higher bond yields which normally signal strengthening inflation and growth. The normally growth sensitive metal price appears to be taking a back seat as an indicator of market conditions for the time being. Its holding pattern may be suggestive of indecision and the possibility of a future break in direction as the global growth trajectory becomes clearer.

Bulk Commodities

Chinese economic growth reports show the national economy meeting its targets, as one would expect for a centrally planned economy, but without any overt signs of upside risk. The tariff fight with the USA is beginning to take a toll on activity rates in an economy with a bias toward less strong growth in the years ahead.

The latest manufacturers purchasing managers index for China, measuring conditions in October, implied continuing slowing in momentum with some evidence of the Sino-US trade dispute taking a toll on conditions.

Growth was slowing in any event leading the Chinese authorities to once again resort to pumping up the economy through more infrastructure spending.

Reported GDP growth in the September quarter was consistent with official forecasts although hitting the targets is becoming more challenging by the year.

Iron ore prices faltered slightly during the week but, among the main mining commodities, are now one of the few sources of metal price strength over the past year.

Coal prices slipped further during the week, albeit after some strong gains. China reported growth in coal output between September and August and over the year to September with plans to open new capacity proceeding as the country switches to larger more efficient sources of coal production.

Oil and Gas

Crude oil prices slumped dramatically as concerns about demand growth loomed and supply constraints appeared looser. A CIA report implicating the Saudi crown prince in the murder of journalist Jamal Kashoggi appeared to give US President Donald Trump some added leverage in his efforts to have the Saudi's keep a lid on prices.

OPEC disclosed in its last monthly market report that it expected demand for crude to grow less strongly in 2019 than it had previously forecast in another sign of the decelerating global economy.

OPEC, and the Saudi government, has also been losing control of the market as US and Russian production has become more significant.

Reimposition of Iranian economic sanctions by the US government had put upward pressure on prices but the US government itslef provided some relief by announcing that it would not apply sanctions against some importers of Iranian oil, at least for the time being.

US production, in any event, continues to rise and is now matching output from Russia and Saudi Arabia. Texas alone is positioned to be the third largest producer after Russia and Saudi Arabia. Export infrastructure limitations may be the greatest impediment to US production having a greater effect on international energy prices.

Rising US stock holdings have impacted the structure of WTI futures prices.

The prices of oil related equities have reacted negatively, as one would expect, to the weakening market conditions with added pressures coming from slumping equity prices during October. Not having responded strongly to the previous rise in crude oil prices, prices of oil and gas exploration and development stocks have shown limited downside leverage to the further weakness in crude oil prices in the past week.

Battery Metals

Eighteen months of rising lithium-related stock prices have given way to a prolonged period of market reassessment as a lengthy pipeline of potential new projects has raised the prospect of ongoing supplies better matching expected needs.

Potential lithium producers have been able to respond far more quickly to market signals than has been the case in other segments of the mining industry where development prospects have been slowed by reticence among financiers to back development.

Movements in lithium related equity prices had been aligned more closely with overall sector equity prices in recent weeks with the lithium stocks tending to display a greater leverage to changes in market sentiment about the mining sector.

The median fall from their 52 week high within a large sample of 80 Australian and Canadian listed stocks with lithium exposure, mostly with an exploration orientation, has exceeded 50%. Every one of the stocks is trading below its peak price from the last year.

Battery metals remain a focal point for investors with recent attention moving to cobalt and vanadium.

Doubts about political conditions in the Democratic Republic of the Congo (and instances of Ebola) have added a dimension to cobalt prices lacking in other metals caught up in the excitement over the longer term impact of transport electrification. Short term market tightness relating to non-battery demand is easing.

In the longer term, cobalt is the most vulnerable of the battery related metals to substitution with high prices likely to stimulate research in that direction.

A spokesperson for Panasonic, manufacturer of batteries for Tesla motor vehicles, has been quoted as saying that the company intends to halve the cobalt content of its batteries because of uncertainties over supply although, offsetting such a move, will be the rapid increase in the number of units produced.

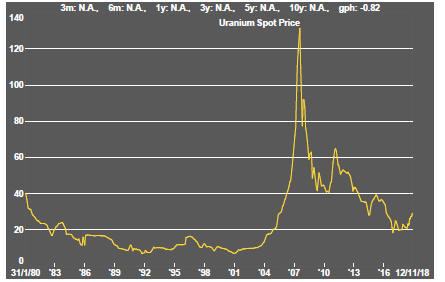

Uranium

The uranium sector is in the midst of forming a prolonged cyclical trough as market balances slowly improve. Power utilities have been reluctant to re-enter the market for contracted amounts of metal to meet longer term needs although an upward bias in prices is now evident.

The effect of an announcement by Canadian producer Cameco to extend the duration of its previously implemented production cut gave the market a very slight but quickly lost lift.

Slightly higher equity prices from time to time, in the hope of improved conditions, have not been sustained but could be repeated as speculation about improved future demand ebbs and flows.

News that the Kazakhstan government intends to list its state owned uranium producer, also the world's largest producer, may suggest greater responsiveness to market conditions and less emphasis on production to maximise government revenue.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.