The Big Picture

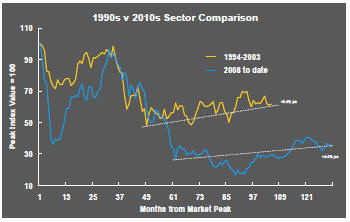

After recovering through 2010, a lengthy downtrend in sector prices between 2011 and 2015 gave way to a relatively stable trajectory similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of frequent macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability in sector prices suggests a chance for individual companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low some 90 months after the cyclical peak in sector equity prices but these conditions were reversed through 2016 and 2017 although, for the most part, sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

In the absence of a market force equivalent to the industrialisation of China, which precipitated an upward break in prices in the early 2000s, a moderate upward drift in sector equity prices over the medium term is likely to persist.

The Past Week

US-China trade talks loomed larger as potent market influences as both parties expressed dissatisfaction with progress.

No further meetings between US and Chinese officials have been scheduled despite the previously optimistic tones from the two parties.

The Chinese appear to have decided that making changes to their laws was one step too far in accommodating the US side. The US side seems to think that the absence of legal changes proves insincerity.

The US government is now raising existing tariffs and moving toward imposing additional tariffs on a full array of Chinese goods, ramping up the potential economic effects of its use of tariffs as a tool to extract negotiation concessions.

At the same time, the US administration is dropping duties on a range of metals imported from Mexico and Canada, possibly as a precursor to a push to have the revamped NAFTA deal approved by the US Congress.

The trade policy focus will then shift to Europe and Japan where it also claims unfair practices affect trade imbalances. The US administration is becoming increasingly desperate for a deal after putting at risk relationships with all its major trading partners.

The apparent failure of US-China trade talks has raised the probability of weakening global growth during 2019. The trade impasse has also set the scene for stronger US consumer price inflation which poses a potential dilemma for Federal Reserve policymakers.

Meanwhile, financial markets are leading expectations toward rate cuts in the later part of 2019. This prospect is helping to sustain US equity markets although, elsewhere, the tone is decidedly more negative.

Emerging market economies will be the most highly leveraged to a downturn in global growth. Exchange rates are beginning to reflect these pressures.

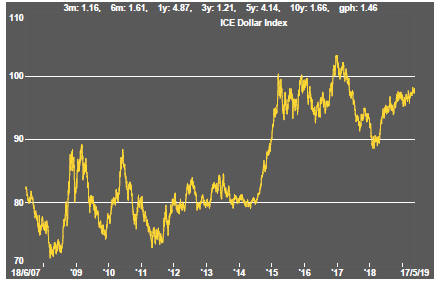

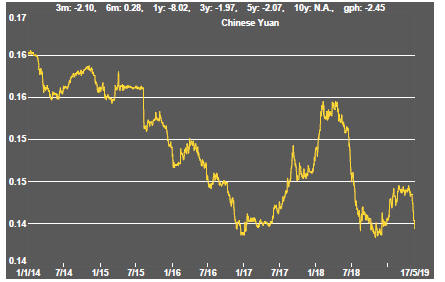

The US dollar continues to edge higher. China’s yuan has moved lower as the trade frictions have intensified.

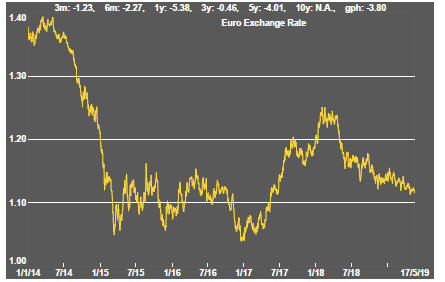

For reasons associated with the failure to pass a European withdrawal Bill, sterling has also fallen.

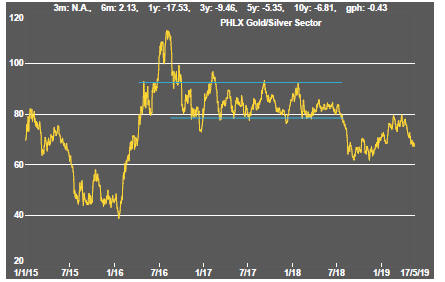

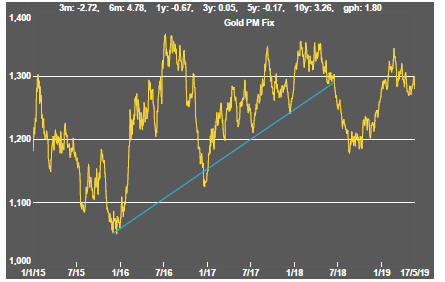

The stronger US dollar – with its negative connotations for US dollar denominated commodity prices - and expectations of stalling global growth have pushed the Australian currency down. Lowered activity will force an easing in Australian monetary policy in due course. More immediately, the weaker Australian dollar has flowed through to stronger pricing for ASX-listed gold companies.

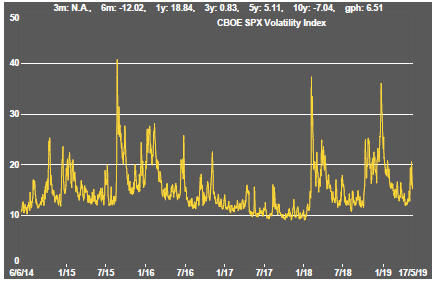

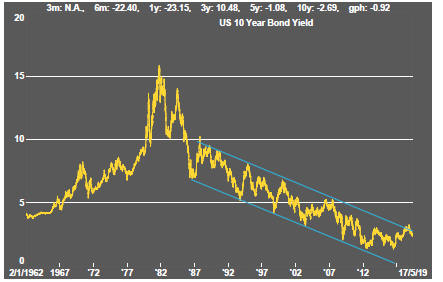

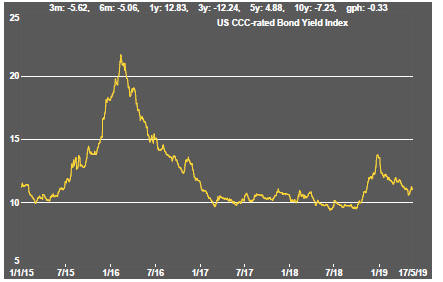

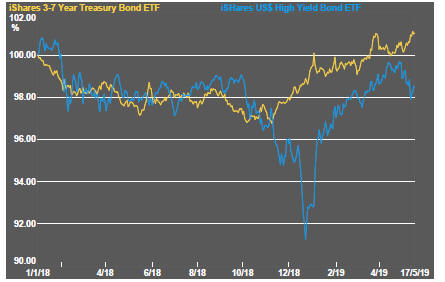

The change in market mood has come with widening spreads between US government securities and high yield corporate bonds. Changes in relative bond prices have negative implications for the availability of mining industry development funds.

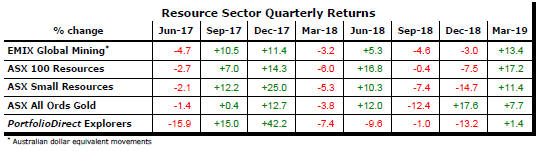

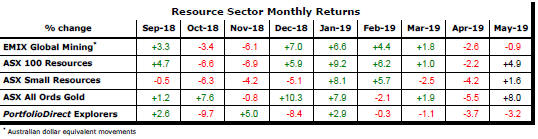

Sector Price Outcomes

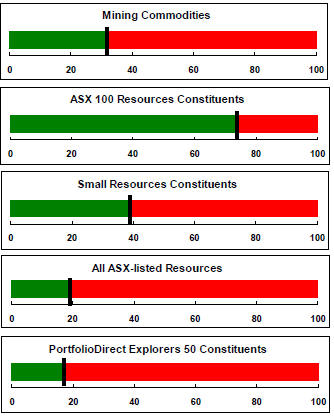

52 Week Price Ranges

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.

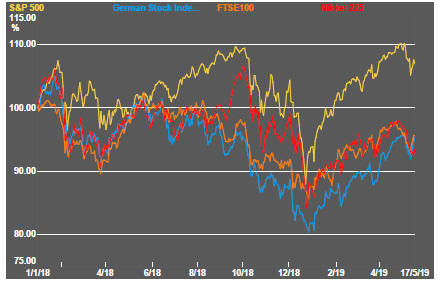

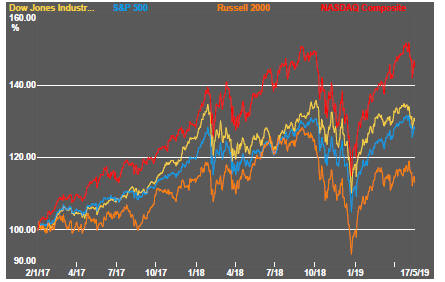

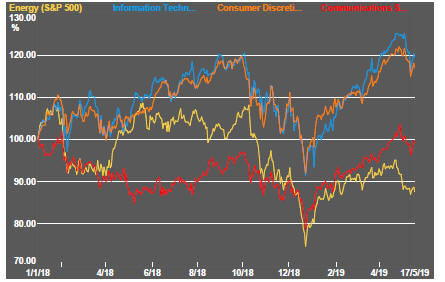

Equity Market Conditions

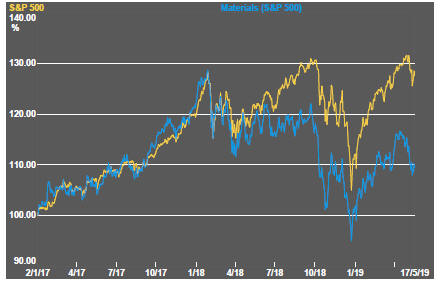

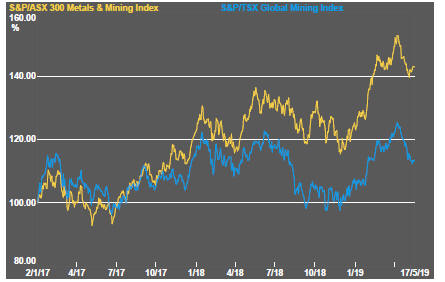

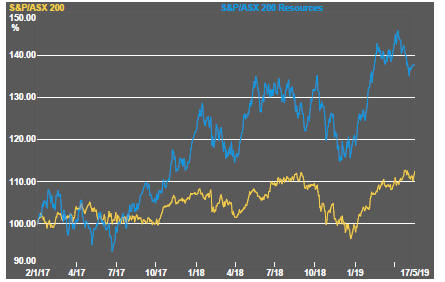

Resource Sector Equities

Interest Rates

Exchange Rates

Commodity Prices Trends

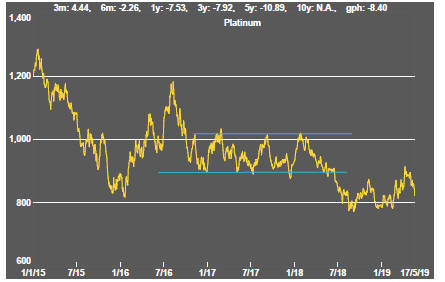

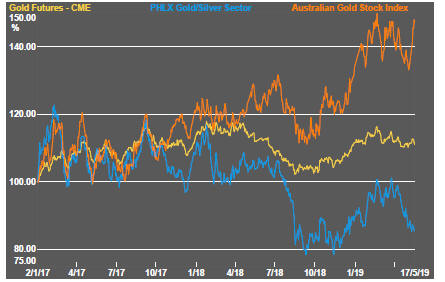

Gold & Precious Metals

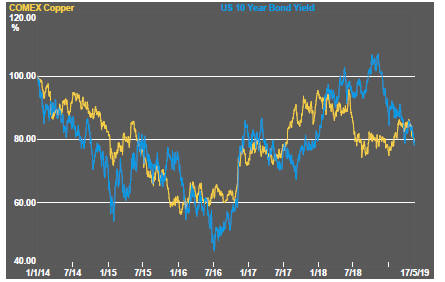

Nonferrous Metals

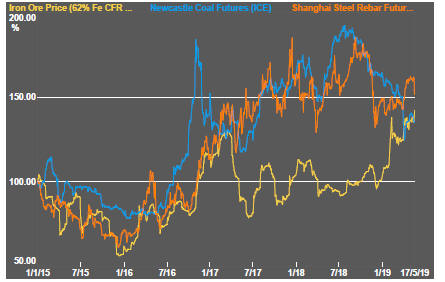

Bulk Commodities

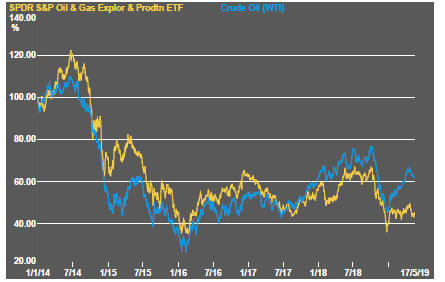

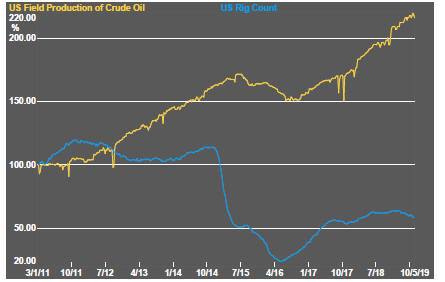

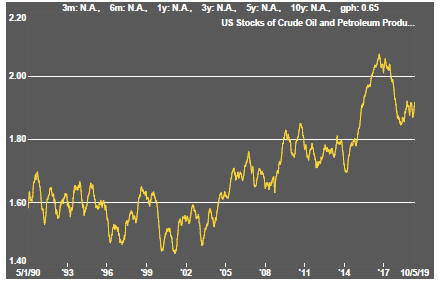

Oil and Gas

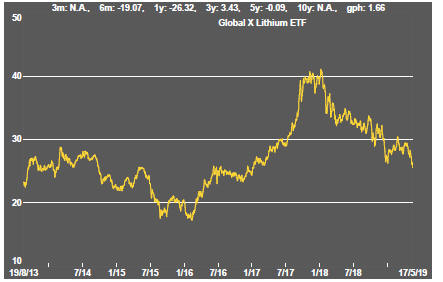

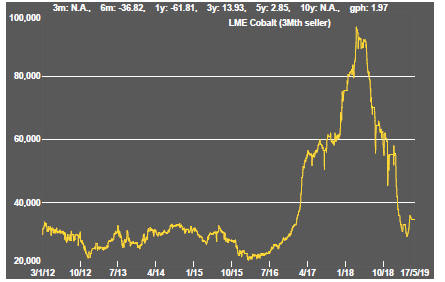

Battery Metals

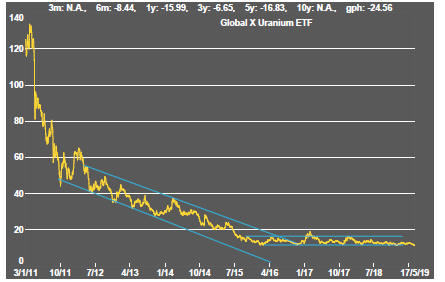

Uranium