The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

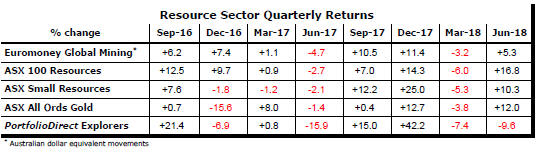

Resource Sector Weekly Returns

Market Breadth Statistics

52 Week Price Ranges

Equity Markets

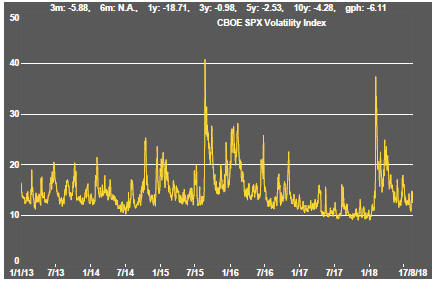

Worldwide equity markets were weaker although the U.S. market remained close to record levels. Emerging market including prices have remained especially weak.

Subdued U.S. market volatility measures continued to suggest relatively few worries on the part of investors despite rising interest rates, imposition of new trade barriers, U.S. political intrigues over pending court cases arising from the 2016 elections and a breakdown of political and economic institutions in several developing countries.

News that China and the USA were to re-commence trade talks, albeit at a junior level, buoyed markets. Mexican government officials continued to speak optimistically about the outcome of trade negotiations with the USA although Canada has not been involved in the latest rounds of NAFTA talks.

President Trump intervened in markets during the week with a suggestion that U.S. companies no longer be required to report quarterly earnings, claiming that the change would encourage a desired longer term perspective in business decision making.

The Trump intervention follows the President’s unorthodox expression of views about monetary policy, suggesting that the Federal Reserve was not as supportive of his policies as he would like.

The President seems unafraid to affect markets with his remarks where his predecessors were less prepared to venture, a risk to bear in mind as the cycle evolves.

Resource Sector Equities

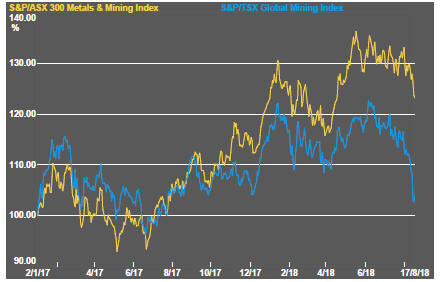

Resource sector prices moved sharply lower with international prices being hit harder than the prices of ASX-listed securities in a sector-wide sell-off. Weaker sector prices were felt across all the development stages of the industry.

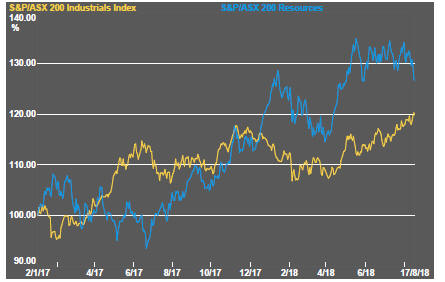

Among ASX listed companies, industrial stock prices continued to outperform resource sector equity prices.

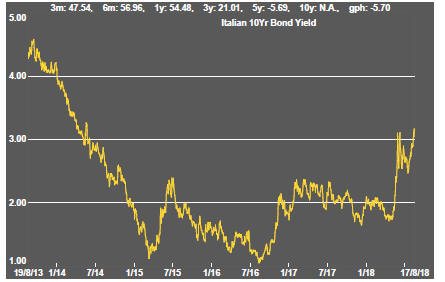

Interest Rates

Risk adjustments continued to feature in financial markets with higher Italian bond yields accompanying lower German yields and little change in US yields.

Corporate financial market conditions with an impact on funding for mine developers remained cyclically attractive.

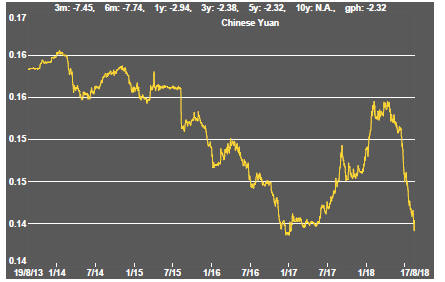

Exchange Rates

The US dollar maintained an upward bias which has reflected capital movements due to a reassessment of risk and expectations about ongoing rises in interest rates.

Sterling, against an ongoing risk of no agreement on the terms of Britain’s post-Brexit relationship with Europe, moved lower as did the euro.

Developing market currencies retained their downward biases although the Turkish lira retrieved some of its recent losses as the government sought to stabilise conditions with promises of support from friendly countries.

The weaker Chinese yuan will have eroded some of the effects of the Trump administration tariff measures - one reason for the President’s expressed irritation about the interest rate policies of the US Federal Reserve.

The Australian dollar has been perceived as an innocent victim in the Sino-US trade crossfire although rising anxieties about the trajectory of Chinese economic activity will also have been sapping some of its strength due to the commodity market connection.

Commodity Prices

The general upswing in commodity prices since mid 2017 had been given added impetus by stronger crude oil prices.

Diminished momentum has left prices within the bounds of a cyclical trough, albeit at the upper end.

The flip side of the benefits for commodity producers and exporters of higher commodity prices is the cost pressure now being experienced by users of agricultural and raw material commodities. Reporting companies have been suggesting this as a source of margin compression.

Business surveys closely watched by central banks are showing signs of upward pressure on selling prices as a result of higher raw material prices.

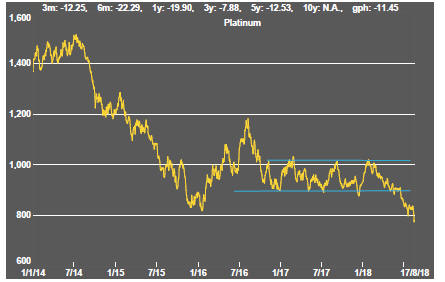

Gold & Precious Metals

Weakening trends in gold and precious metal prices persist.

Looked at against broader financial market conditions, gold had appeared overpriced and at risk of a significant reversal. Further bond price falls are likely to aggravate the trend.

Across the precious metal sector, prices have broken through the bounds of prior trading ranges.

Gold and palladium price uptrends have been broken. Platinum prices fell below the lower bound of a two year trading range. Silver prices which had proved relatively resilient have been caught up in the trend to weaker prices.

The divergence in trend between Australian and north American gold related equities has persisted with the size of the gap suggestive of future relative underperformance among the Australian branch of the market.

Nonferrous Metals

The major daily traded nonferrous metal prices are converging on some of the lowest levels of the past year. The highly correlated moves suggest little opportunity for differentiation among individual metals due to any peculiar circumstances.

Industry statistics continue to signal that higher prices have been driven by unusually weak demand mitigated by lowered production rates leaving them at risk of reversal as new supplies enter the market in response to price incentives.

Much of the commentary about the decline in copper prices has focused attention on the impact of trade policy. There will have been some effect from this source but prices had shown little net change for the best part of a year amidst a clear loss of momentum before the trade policy issue began to gain traction.

The performance divergence between the copper price and US bond yields suggesting less bullishness within the copper market about the growth outlook might be consistent with the relatively muted response on the part of market yields to the rise in interest rates by the Federal Reserve.

Nonferrous metal prices have been caught up in rising worries about Chinese economic activity in part because of the anticipated impact of US trade policies but also due to Chinese government initiatives to curb excessive lending.

Bulk Commodities

Relatively weak first quarter Chinese GDP growth had suggested a ramp up in activity through the remainder of 2018 if China was going to meet its growth target which, in a centrally controlled economy in which leaders are trying to maintain credibility, is a reasonable assumption.

The difficultly of achieving its targets has now been acknowledged by Chinese officials who have conceded that second half growth may not be as strong as had been expected.

Nonetheless, the Chinese government reported a June quarter GDP growth in line with its stated target.

Coal prices have remained firm with demand from China growing at its fastest pace since 2011. Indian port authorities have also reported strong growth in coal movements in the second quarter of 2018. Prices have been supported, too, by constraints on supply imposed by financial institutions unwilling to support mine development.

Iron ore prices have remained largely unresponsive to improved demand for steel and ongoing expansion of Chinese manufacturing output until the last fortnight when prices have pushed higher.

Oil and Gas

The upward trend in crude oil prices has given way to a leveling out in prices following recent price falls, including during the past week.

While a meeting of OPEC members decided to expand production, the size of the increase was less than had been expected helping to maintain upward pressure on prices. Meanwhile, the push by the US administration to re-impose economic sanctions on Iran was also working to keep prices risisng.

The Iranians have been lobbying European countries to prevent more widespread application of sanctions but the likelihood of relief appears slim as long as funds must circulate through US banks.

US production, in any event, continues to rise and is now matching output from Russia and Saudi Arabia. Texas alone is positioned to be the third largest producer after Russia and Saudi Arabia.

Despite the change in tone within crude oil markets, related equity prices have been muted in their responses, implicitly signaling scepticsm about the sustainability of price rises.

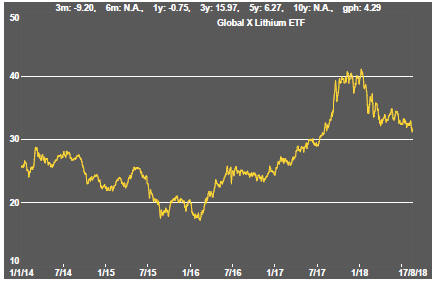

Battery Metals

Eighteen months of rising lithium-related stock prices has given way to a period of market reassessment as a lengthy pipeline of potential new projects has raised the prospect of ongoing supplies better matching expected needs.

Potential lithium producers have been able to respond far more quickly to market signals than has been the case in other segments of the mining industry where development prospects have been slowed by reticence among financiers to back development.

Movements in lithium related equity prices hade been aligned more closely with overall sector equity prices in recent weeks although they have not suffered the wider sector sell-off in the past week.

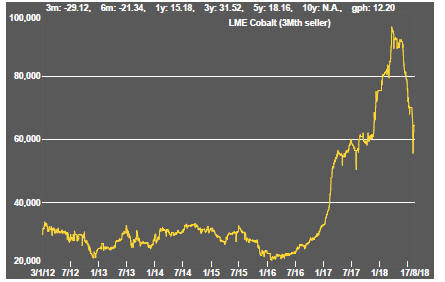

Battery metals remain a focal point for investors with recent attention moving to cobalt and vanadium.

Doubts about a peaceful transfer of political power in the Democratic Republic of the Congo (and instances of Ebola) have added a dimension to cobalt prices lacking in other metals caught up in the excitement over transport electrification. Improved political conditions left cobalt prices at risk of some retracement - as has recognition that the surge in future needs for battery storage did not warrant the near term price action which reflected more on shortages for traditional uses.

In the longer term, cobalt is the most vulnerable of the battery related metals to substitution with high prices likely to stimulate research in that direction.

A spokesperson for Panasonic, manufacturer of batteries for Tesla motor vehicles, has been quoted as saying that the company intends to halve the cobalt content of its batteries because of uncertainties over supply.

Uranium

The uranium sector is in the midst of forming a prolonged cyclical trough as market balances slowly improve. Power utilities are still not prepared to re-enter the market for contracted amounts of metal to meet longer term needs. A slight upward bias in prices has been evident in the past month.

Slightly higher equity prices from time to time, in the hope of improved conditions, have not been sustained but could be repeated as speculation about improved future demand ebbs and flows. The effect of an announcement by Canadian producer Cameco to extend the duration of its previously implemented production cut gave the market a very slight but quickly lost lift.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.