The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

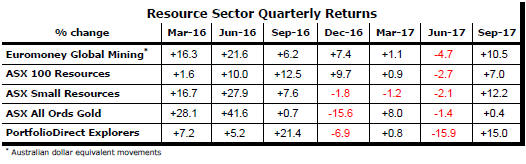

Resource Sector Weekly Returns

Market Breadth Statistics

Near record equity prices across all major as well as emerging markets persisted through the past week helped by a combination of favourable earnings, a less risky global growth picture, improving commodity prices, still supportive monetary policies and, in the USA, expectations of tax cuts for corporations.

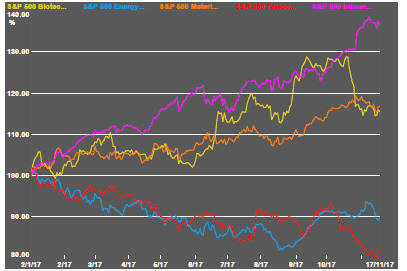

Despite the overall market strength, the leading sectors of the US market have moved lower in recent weeks with only the information technology group, comprising some of the most rapidly growing and highest profile companies, remaining very near peak levels.

The US bond market continues to imply doubts about the growth outlook and the likelihood of a meaningful increase in inflation. Against his background, the drive to higher short term interest rates confirm that policy rate adjustments are being driven by a wish to prepare for the next cycle rather than dealing with current conditions.

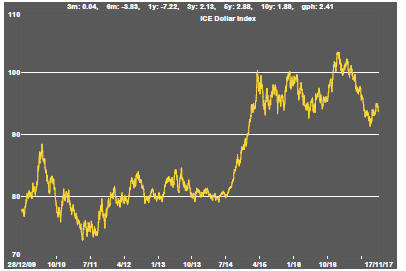

The US dollar slipped back slightly as some doubts emerged about the likely speed and content of the US tax reform process.

From a raw material market perspective, the exchange rate and financial market variables are suggesting a loss of forward momentum which had been relying previously on a weakening currency and lower interest rates.

The high yield market (also depicted in chart 6 in the panel on the right) took a turn for the worse from the perspective of the resources sector.

The fall in corporate bond prices or the rise in yields suggests a slightly reduced willingness to embrace risk.

The change in direction is not strong enough to destabilise markets but is another indicator suggesting some loss in momentum toward the end of the year.

Sentiment could change once again with progress in tax cutting in the USA to which smaller more risky companies would be leveraged.

With separate legislation moving through the two houses of the US Congress, attention will turn to how readily the differences can be reconciled between the two bodies with the Democrats in both houses universally opposed to any changes being proposed.

The major daily traded nonferrous metal prices have all moved lower with these and other key commodities for the mining industry sitting around 70% through the range of price outcomes over the past 52 weeks.

Only the tin price has changed little as these adjustments have been occurring.

In the absence of large changes in government bond prices, gold bullion prices have also tended to become less volatile.

Gold related equities have appeared less responsive to bullion price movements and are nearing the lower end of the trading range established over the past year.

Within the gold sector, Australian listed gold stocks have performed more strongly than those on north American markets, helped by a weaker Australian dollar and some rising bullishness about the discovery potential within Australia.

Crude oil prices have been gaining strength in anticipation of an extension of the existing agreement among some of the major producers to curtail supply. That said, the market remains trapped cyclically as supplies from countries not participating in the production shedding agreement continue to respond to any improvement in prices.

The apparent loss of commodity price momentum and doubts about the Australian growth picture have led to the Australian dollar retracing gains made through the middle of 2017.

The change in direction should make Australian equities more attractive to overseas investors who are, based on past experience, likely to wait until the fall has run its course rather than attempt to preempt a turn.

.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.