The Big Picture

After recovering through 2010, a lengthy downtrend in sector prices between 2011 and 2015 gave way to a relatively stable trajectory similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of frequent macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability in sector prices suggests a chance for individual companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low some 90 months after the cyclical peak in sector equity prices but these conditions were reversed through 2016 and 2017 although, for the most part, sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

In the absence of a market force equivalent to the industrialisation of China, which precipitated an upward break in prices in the early 2000s, a moderate upward drift in sector equity prices over the medium term is likely to persist.

The Past Week

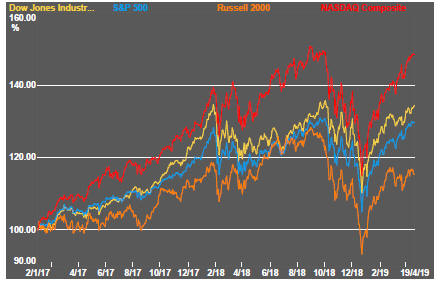

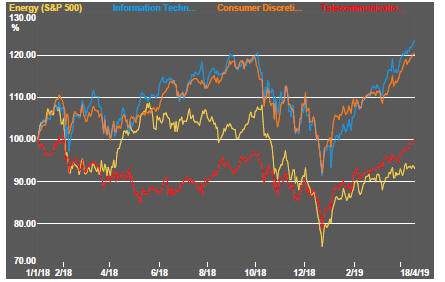

Market conditions reflected a continuation of the influences which have prevailed since the commencement of 2019. Pivotal to the improved equity markets has been a switch in central bank thinking about the appropriateness of their policy settings.

Investors are pricing equities as though realisation of evident downside risks is unlikely.

The biggest market risk - a slowdown in global economic conditions - would have a particularly adverse effect on metal commodity markets and related company equities.

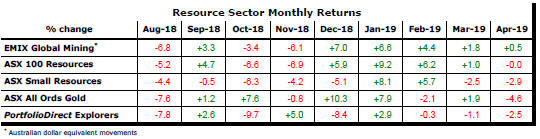

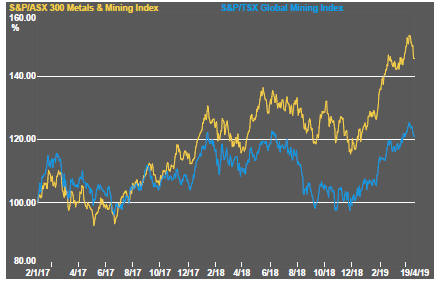

Against the trend in headline equity indices, metal prices and related stock prices lost momentum during the past week.

The pattern of metal price movements remains consistent with cyclical decline.

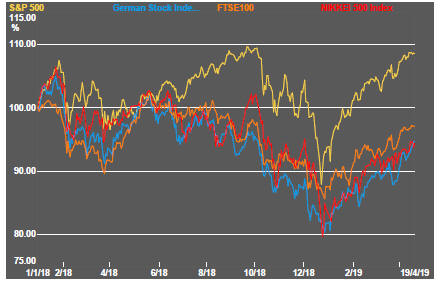

The sector leaders continue to outperform the vast bulk of companies within the sector. Prices of explorers remain anchored near historically low levels.

The direction of interest rates continues to favour the outlook for mining projects provided they can demonstrate fundamentally sound investment propositions.

A tug-of-war is underway between the key influences on metal market conditions. Global economic growth is slowing after several years of already unusually slow growth in metal demand. At the same time and on the other side of the balance, metal supplies are heavily constrained, averting a depressing effect on metal prices through what would have otherwise been a significant accumulation of inventories.

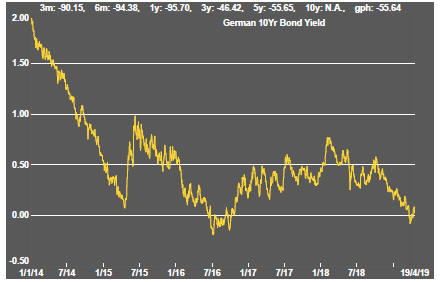

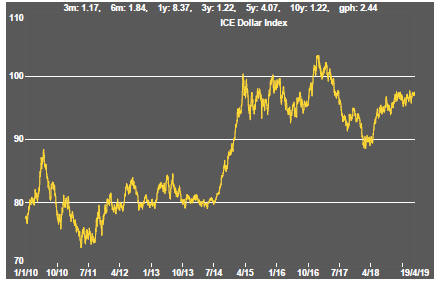

US dollar strength is currently putting a lid on metal price movements. The possibility of an eventually lower US dollar remains the most potent potential contributor to possibly higher metal prices or a limitation on the extent to which prices might fall.

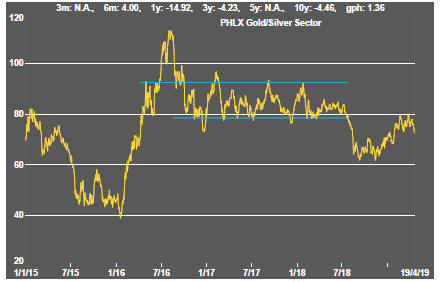

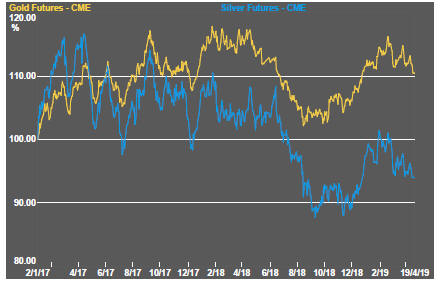

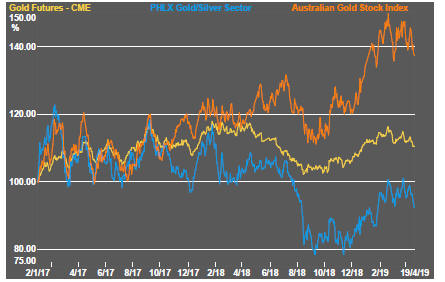

Gold prices are in retreat after having failed to break above previous high prices set over the past three years. A bias toward low interest rates would also be a contributor to lower gold prices.

Australian gold equities which had significantly outperformed the gold price in late 2018 are beginning to face a downside threat.

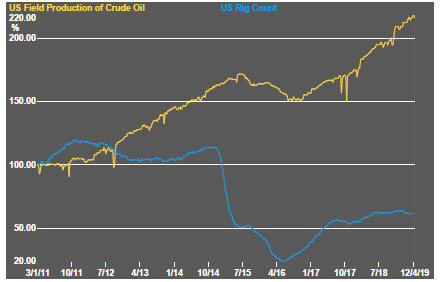

Significantly elevated oil prices as a consequence of supply constraints, including tightening sanctions on Iranian exports, have not so far been reflected in equity price movements for oil and gas exploration and production stocks. The implied scepticism of investors will have to be reconciled in due course.

Sector Price Outcomes

52 Week Price Ranges

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.

Equity Market Conditions

Resource Sector Equities

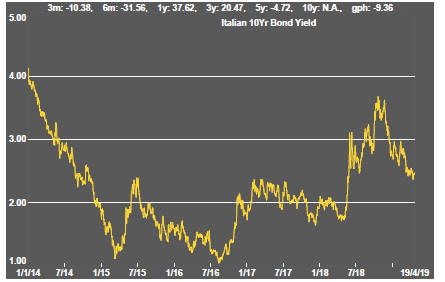

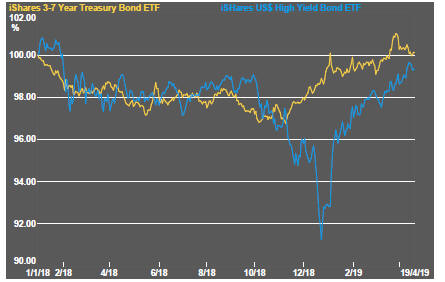

Interest Rates

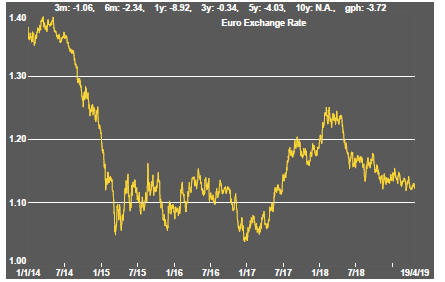

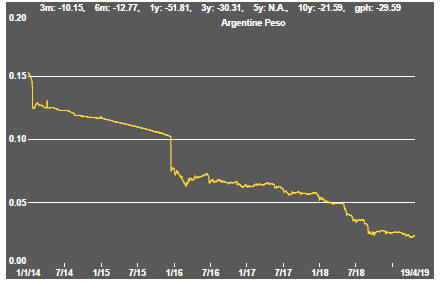

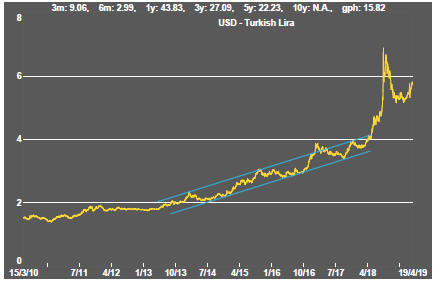

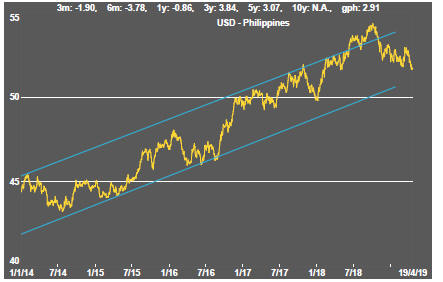

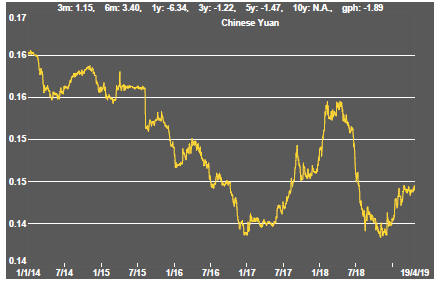

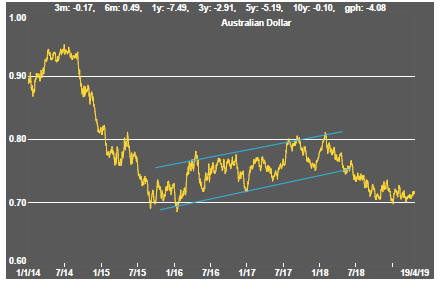

Exchange Rates

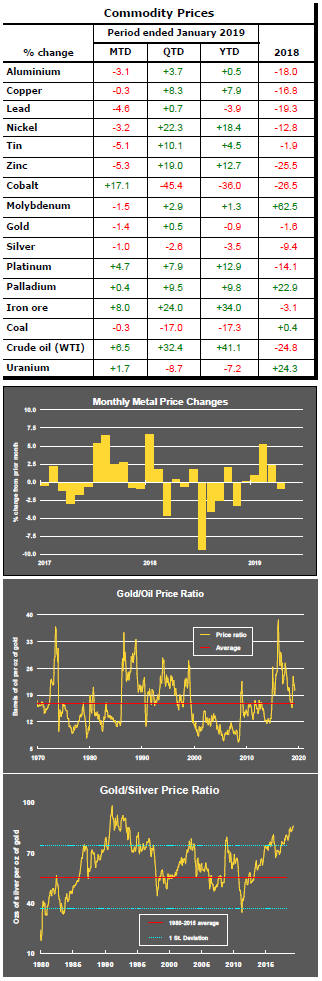

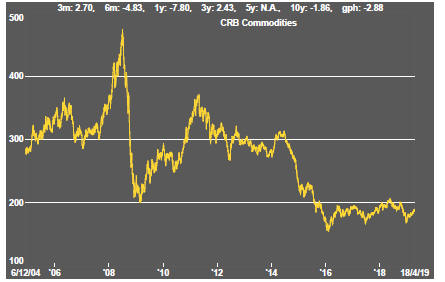

Commodity Prices Trends

Gold & Precious Metals

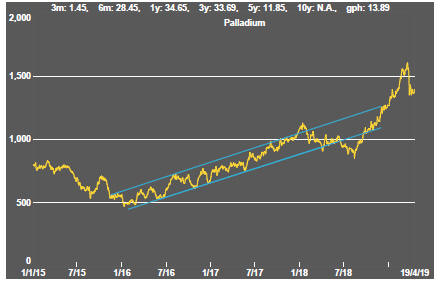

Nonferrous Metals

Bulk Commodities

Oil and Gas

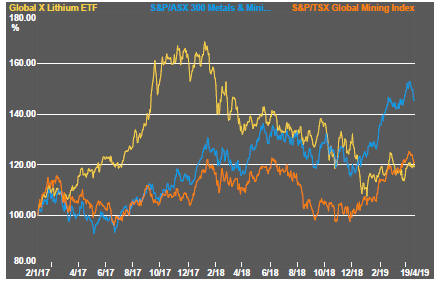

Battery Metals

Uranium