The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

Resource Sector Weekly Returns

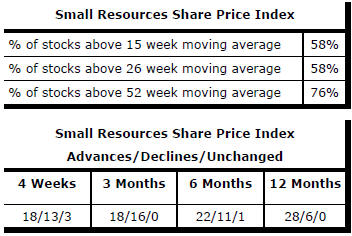

Market Breadth Statistics

52 Week Price Ranges

Equity Markets

Generally weakening equity prices over the past week papered over some divergent trends across mrkets.

Globally, the slump in emerging market prices has worsened. Peculiar structural and political problems in a range of countries meant each could be looked at independently, at least in the early stages of the sell off. Then, higher oil prices became a common issue for the oil importers. Shortly afterwards, anxiety over the synchronised global growth theme failing to eventuate aggravated the investor response.

Within the US market, international conditions are fostering an apparent preference for domestically oriented smaller companies, helping to propel the Russell 2000 index.

The disruptive effect of US trade policy decisions is worsening as more companies cite uncertainty about outcomes as a reason to postpone investment decisions.

The US administration has become even less adept at explaining the rationale for its approach and the benefits which are likely to ensue, adding to growing frustration even among companies that had once supported action against imports from China.

Resource Sector Equities

Material sector prices remain within their uptrend while moving toward the lower bound of the range. Overall, returns for miners during the week were negative.

In the Australian context, the industrial sector has been running ahead of the resources component of the market.

Australian gold stocks have outpaced the bullion price and the prices of north American peer companies as the Australian dollar has lost ground against the US currency.

The smallest stocks in the sector once again fared worst as the trend away from risk assets filtered through the resources sector. Many will have also suffered from the seasonal effect accompanying the end of the financial year.

Interest Rates

US 10 year bond yields remained under the 3% barrier helping to shore up equity market prices.

Market rates have generally eased with less concern about European fiscal conditions and, within that trend, a continuing demand for less risky assets such as those of Germany and the USA.

Low rated corporate bond yields edged lower suggesting some of the best industry financing conditions in over a year.

Exchange Rates

The broad currency trends of the past several weeks favouring the US dollar continued although the upward move of the US currency has been less marked over the past two weeks.

A move lower by the Chinese yuan was more dramatic as some speculated that Chinese authorities may have been giving their companies some breathing space to ease pressures from a tariff battle with the US government.

Developing country exchange rates continued to face downward pressure. Individual differences in the causes of currency weakness have started to merge into a theme into which the Australian dollar has been pulled.

The Australian currency appears to have fallen out of an upward trend which dates from early 2016 with a threat of the trade with the US dollar reverting to where it had been in late 2015.

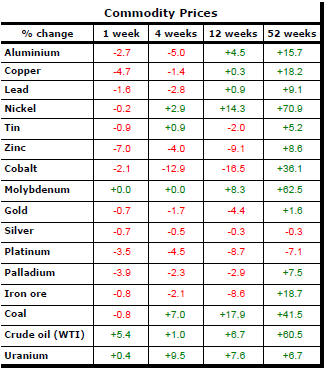

Commodity Prices

The general upswing in commodity prices since mid 2017 had been given added impetus by stronger crude oil prices.

Prices remain within the bounds of a cyclical trough, albeit at the upper end.

The flip side of the benefits for commodity producers and exporters of higher commodity prices is the cost pressure now being experienced by users of agricultural and raw material commodities. Reporting companies have been suggesting this as a source of margin compression.

Business surveys closely watched by central banks are showing signs of upward pressure on selling prices as a result of higher raw material prices.

Gold & Precious Metals

Across the precious metal sector, prices had started to push against the bounds of prior trading ranges.

Over the week, the gold and palladium price uptrends were broken. Platinum prices fell below the lower bound of a two year trading range. Silver prices proved the most resilient in staying within its trading range.

The divergence in trend between Australian and north American gold related equities remains evident with US markets more aligned with a sceptical view of the near term future of precious metal prices and the Australian market helped by a weaker Australian dollar.

Nonferrous Metals

Metal prices were heading sharply lower at the end of the week amid signs of poorer than previously expected growth outcomes and, somewhat related, concerns about the effect of a trade clash between the US government and most of its trading partners.

Prices of the main daily traded nonferrous metals had previously broken into three groups. Group one comprised those metals affected by US sanctions on Russian economic and political interests, namely nickel and aluminum. The second group included those metals being driven by broader macro trends which are showing up as a loss of growth momentum. The third category comprised tin alone.

Nickel prices have remained strong but, otherwise, signs of convergence and the dominance of broader macro factors, have re-emerged.

Scepticism about the growth trajectory embedded in bond yield movements is now also being reflected more clearly in copper prices which remain consistent with building pressure for a cyclical turn although it might be too early to draw a firm conclusion about that from recent price action.

Bulk Commodities

Relatively weak first quarter Chinese GDP growth had suggested a ramp up in activity through the remainder of 2018 if China was going to meet its growth target which, in a centrally controlled economy in which leaders are trying to maintain credibility, is a reasonable assumption.

Iron ore prices have failed to reflect the ongoing expansion in Chinese manufacturing output although coal and steel prices have been climbing.

Oil and Gas

Crude oil prices had reached the highest levels in several years before breaking lower after comments from major producers that a production increase might be contemplated and reports of Russian president Vladimir Putin saying that a $60/bbl oil price would be adequate.

The sharp market response to the slightly more bearish tone might have led to some reconsideration of any plans to push output higher.

While a meeting of OPEC members decided to expand production, the size of the increase was less than had been expected leading to a sharp rise in crude oil prices at the end of the week.

US production, in any event, continues to rise. US producers are able to profitably hedge anticipated production contributing to the ongoing rise in their output.

US production is now matching output from Russia and Saudi Arabia.

Battery Metals

Eighteen months of rising lithium-related stock prices gave way to a period of market reassessment as a lengthy pipeline of potential new projects raised the prospect, although not conclusively, of ongoing supplies being adequate for expected needs.

Potential lithium producers have been able to respond far more quickly to market signals than has been the case in other segments of the mining industry with development prospects.

Movements in lithium related equity prices have been aligned more closely with overall sector equity prices in recent weeks.

Battery metals remain a focal point for investors with recent attention moving to cobalt and vanadium.

Doubts about a peaceful transfer of political power in the Democratic Republic of the Congo (and an Ebola outbreak) added a dimension to cobalt prices lacking in other metals caught up in the excitement over transport electrification. Improved political conditions leave cobalt prices at risk of some retracement.

In the longer term, cobalt is the most vulnerable of the battery related metals to substitution with high prices likely to stimulate research in that direction.

Uranium

The uranium sector is forming a cyclical trough as market balances slowly improve. Power utilities are still not prepared to re-enter the market for contracted amounts of metal to meet longer term needs. A slight upward bias in prices was evident in the past month.

Slightly higher equity prices from time to time, in the hope of improved conditions, have not been sustained but could be repeated as speculation about improved future demand ebbs and flows.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.