The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

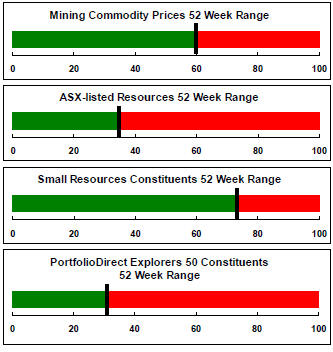

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

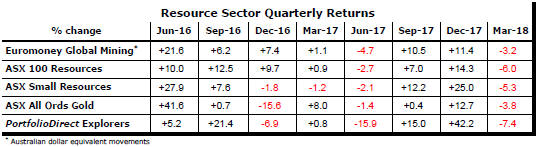

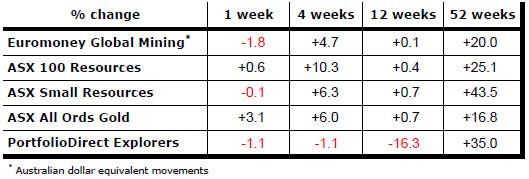

Resource Sector Weekly Returns

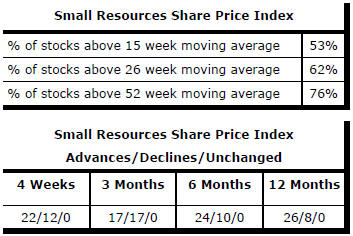

Market Breadth Statistics

Equity Markets

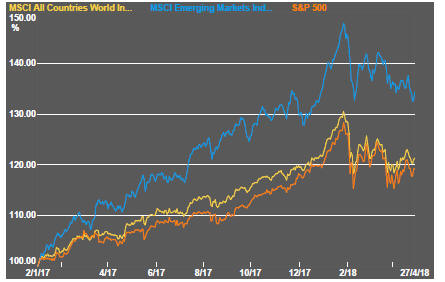

US equity markets faced pressures from rising bond yields, threats of trade wars and middle east political tensions but improved earnings have been expected to carry prices higher.

An above average number of reporting companies have beaten earnings estimates for the March quarter without greatly impacting the overall market, a worrying sign.

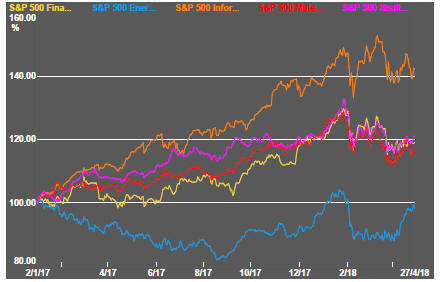

Some of the best performing parts of the US market, such as the energy sector, have had relatively small weightings.

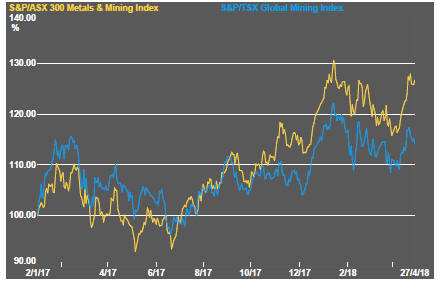

The overall resources sector finished the week moving higher but prices seem to have stalled after a strong rise which had restored prices close to the late 2017 peak values.

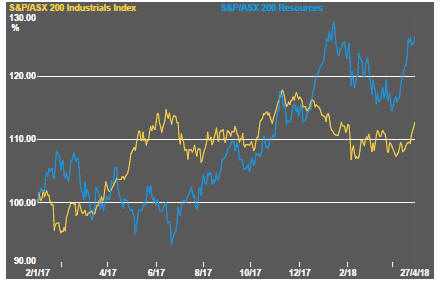

Industrial company share prices outpaced resources sector prices, in the Australian market, in the past week.

Interest Rates

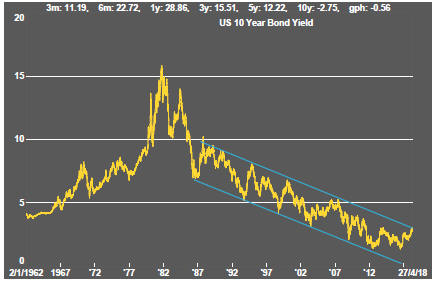

US 10 year bond yields edged through 3%, a level which had become a focus of attention.

The higher levels were more symbolic than economically significant but signified some worries about inflation rising and how the Federal Reserve might react. That is likely to be an ongoing concern as, at some time, yields are poised to break the downtrend which has persisted for some 30 years.

Financial market indicators with implications for funding of the resources sector have shown little change

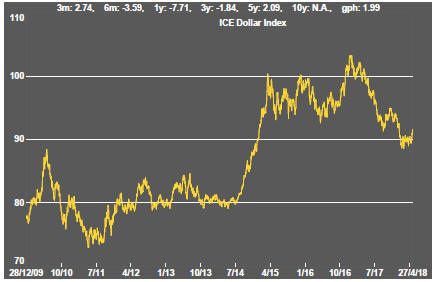

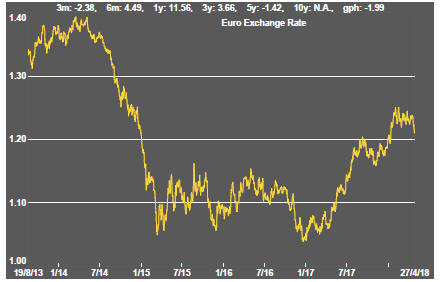

Exchange Rates

Unusually large movements in exchange rates were evident after the US dollar decline had appeared to stall in recent weeks.

The rise in the US dollar came amid rises in US bond yields and some change in sentiment about the need to raise interest rates in Europe where some of the optimism about the growth outlook had begun to ebb.

The stronger US dollar will have had a dampening effect on earnings among the largest US companies albeit against a backdrop of favourable changes in tax rates for corporates.

The gentle upward drift in the Australian dollar could remain intact as long as risks to global economic conditions remain lowered and commodity prices are in the upper end of the range of prices in the past year. That said, the Australian dollar is near the bottom of its trading range and at risk of moving lower.

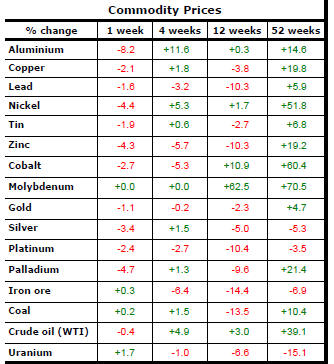

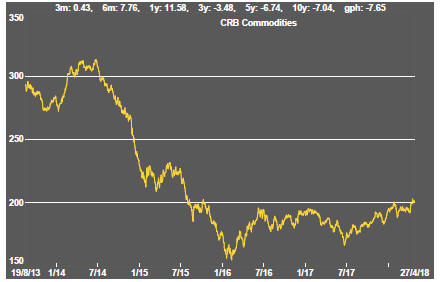

Commodity Prices

The general upswing in commodity prices over the past year remains within the bounds of a cyclical trough suggesting still stronger economic activity will be needed if the cycle is to strengthen. Unusually strong gains in the past fortnight have reflected higher crude oil prices.

Gold & Precious Metals

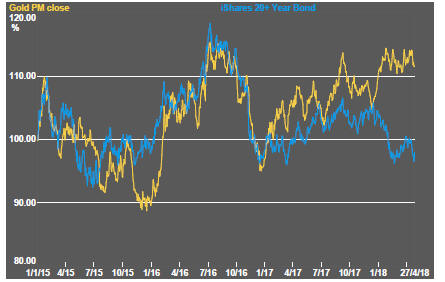

Gold bullion prices remained toward the upper end of their recent range despite the fall in bond prices which, more often than not, would signify a fall in bullion prices.

Silver prices which have been at an extreme low relative to gold prices had risen two weeks ago amidst forecasts of a likely reversal in the gold/silver price ratio toward historical averages.

With the turn in financial market conditions, both gold and silver prices lost momentum although the downward pressure on silver prices appears to be nearing a decision point.

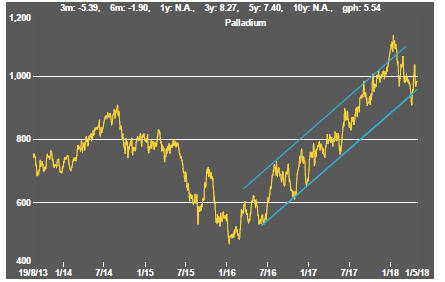

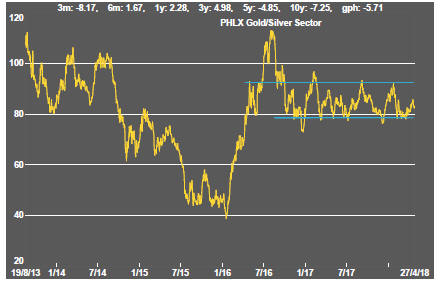

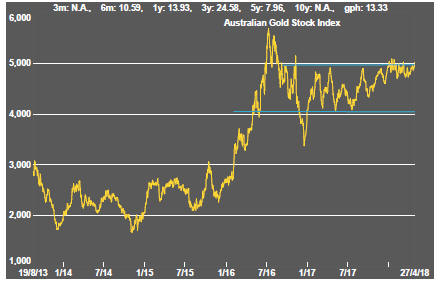

US precious metal equities traded lower after having lifted briefly from near the bottom of their medium term trading range. Australian gold equity prices remained close to the upper end of their trading range with diminished volatility.

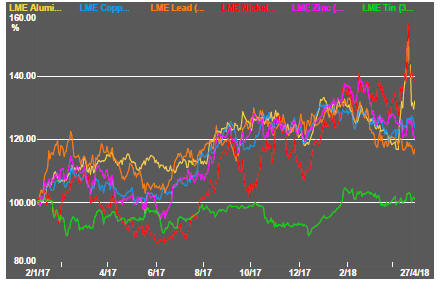

Nonferrous Metals

Prices of the main daily traded nonferrous metals had become increasingly correlated as a broadening consensus about the lowered risks to world economic activity emerged - until the new US sanctions against Russian business interests dramatically impacted aluminium and nickel prices.

With comments from the US administration suggesting that the sanctions will not affect metal supplies as severely as had first been suspected, the two metals most affected retraced their sharp gains. That aside, strong evidence of price convergence remains a feature of the market with only tin prices staying aloof from the crowd.

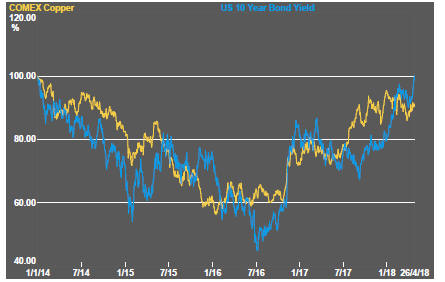

Copper prices again failed to react to the re-pricing of financial assets in the way one might expect to occur if higher bond yields reflect a positive reconsideration of the growth outlook.

Bulk Commodities

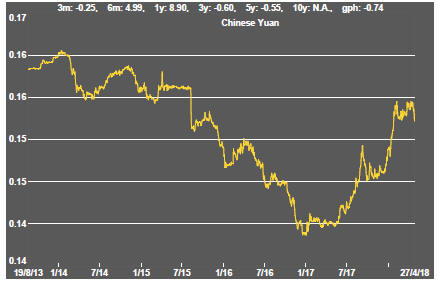

Bulk commodity prices had moved lower with signs of lessening Chinese economic momentum after the first quarter.

Increased Chinese steel production in the first quarter of 2018 has resulted in larger inventories. The inventory climb and threat of tariffs affecting Chinese steel demand have dragged steel prices lower and raised risks for metallurgical coal markets.

A slight reversal of those near term trends has been evident in the past two weeks.

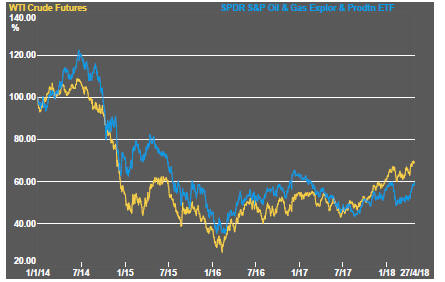

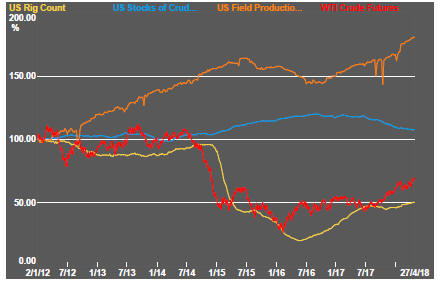

Oil and Gas

Rising US production, partly in response to higher prices, had been seen as a burden on expectations about the likelihood of further oil price rises.

US producers are also now able to profitably hedge anticipated production contributing to the ongoing rise in their output.

On the other side of the ledger, inventories have been declining and global supplies have remained constrained through both voluntary and involuntary actions. Fears of deteriorating political conditions in the middle east have also elicited a higher risk premium.

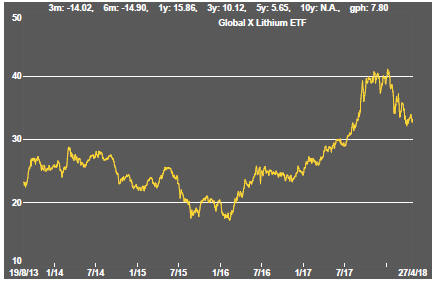

Battery Metals

Eighteen months of rising lithium-related stock prices have given way to a period of market reassessment as a lengthy pipeline of potential new projects raises the prospect, although not conclusively, of ongoing supplies being adequate for expected needs.

Potential lithium producers have been able to respond far more quickly to the various market signals than has been the case in other segments of the mining industry.

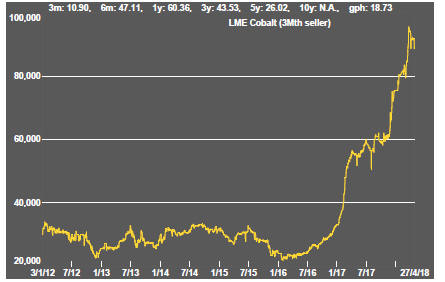

Battery metals remain a focal point for investors with recent attention moving to cobalt and vanadium.

Uncertainty over how a peaceful transfer of power can occur in the Democratic Republic of the Congo has added a dimension to cobalt prices lacking in other metals caught up in the excitement over transport electrification.

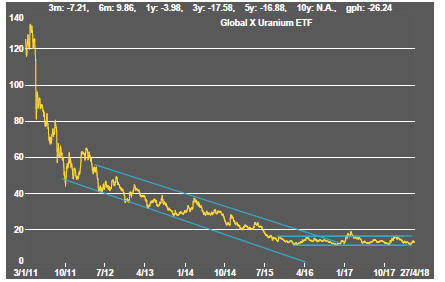

Uranium

The uranium sector is moving along the bottom of its long term trading range in the absence of more meaningful signs that power utilities are prepared to re-enter the contract market to negotiate their longer term needs.

Slightly higher equity prices in the last week could be attributed to speculative trading since uranium prices have moved slightly lower since the end of March.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.