The Current View

Growth in demand for raw materials peaked in late 2010. Since then, supply growth has continued to outstrip demand leading to inventory rebuilding or spare production capacity. With the risk of shortages greatly reduced, prices have lost their risk premia and are tending toward marginal production costs to rebalance markets.

To move to the next phase of the cycle, an acceleration in global output growth will be required to boost raw material demand by enough to stabilise metal inventories or utilise excess capacity.

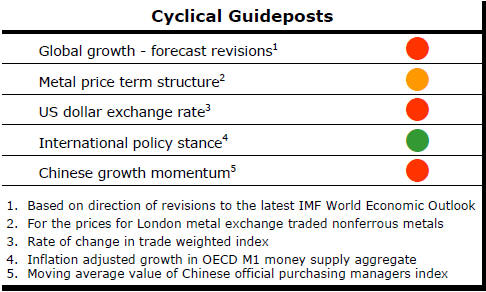

The PortfolioDirect cyclical

guideposts suggest that the best possible macroeconomic circumstances for

the resources sector will involve a sequence of upward revisions to

global growth forecasts, the term structure of metal prices once again

reflecting rising near term shortages, a weakening US dollar, strong money

supply growth rates and positive Chinese growth momentum. Only one of

the five guideposts is "set to green" suggesting the sector remains confined

to the bottom of the cycle .

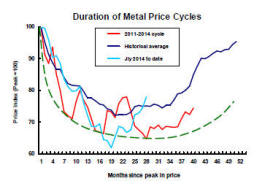

Has Anything Changed? - Updated View

Since mid 2014, the metal market cyclical position has been characterised as ‘Trough Entry’ as prices have remained in downtrend with all but one of the PortfolioDirect cyclical guideposts - the international policy stance - flashing ‘red’ to indicate the absence of support.

The absence of a global growth acceleration, a stronger dollar and flagging Chinese growth momentum remain critical features of the current cyclical positioning.

Through February 2016, the first signs of cyclical improvement in nearly two years started to emerge. After 15 months of contango, the metal price term structure shifted to backwardation reflecting some moderate tightening in market conditions.

The metal price term structure is the most sensitive of the five cyclical guideposts to short term conditions and could, consequently, quickly reverse direction. Nonetheless, this is an improvement in market conditions and the guidepost indicator has been upgraded to ‘amber’ pending confirmation of further movement in this direction.

Mining Development Risk Blindness

Many associated with the resources industry blame cyclical weakness and

accompanying capital shortages for poor investment returns from the

resources industry.

These will have been factors in the investment outcomes, to some extent, but other risky market sectors have been able to tap capital markets. There has been no shortage of capital to invest especially with low interest rates and ample liquidity.

One little mentioned constraint on the mining industry being able to access capital more easily is its risk profile.

There is empirical and theoretical evidence suggesting that investment risks are being underestimated for those companies that have passed through the exploration stage and looking to develop a mining project.

Below is the text of a column recently published by Mining Journal which highlights the tendency for companies and investors to overstate the likelihood of projects being completed and, consequently, underestimate the frequency of investor disappointment.

Daniel Kahneman should be cited in every investment pitch by mining industry executives to show they understand their project risks.

Kahneman, a psychologist, received a Nobel Prize in economics in 2002 “for having integrated insights from psychological research into economic science, especially concerning human judgement and decision-making under uncertainty”, according to the award committee.

Much of Kahneman’s research was conducted with Amos Tversky, another cognitive psychologist, whose collaboration could not be recognised by the Nobel awards committee because he had died of cancer prematurely in 1996.

In the early 1970s, Kahneman and Tversky began to highlight what appeared as sometimes irrational decision making and inexplicably erroneous thought processes by individuals confronted with uncertainty in markets.

Their experiments showed that people were prone to take some decisions even when results ran counter to their own best interests and in defiance of what may have been known about likely outcomes. The decision-making errors arose from a systematic bias in the way in which human minds process risk.

In a paper entitled ‘Judgment Under Uncertainty: Heuristics and Biases’ in Science (Vol 185, pp 1124-1131,1974), the two psychologists described how “people rely on a limited number of heuristic principles, which reduces the complex tasks of assessing probabilities and predicting values to simpler judgmental operations”.

Kahneman and Tversky described these heuristics or rules used to simplify complex decision-making problems as “quite useful, but sometimes they lead to severe and systematic errors”. The 1974 paper is a catalogue of explanations for apparently irrational decision-making outcomes.

While neither Kahneman nor Tversky appear to have thought explicitly about investment decision-making within the mining industry, their discussion of “biases in the evaluation of conjunctive and disjunctive events” has a direct bearing on industry decisions and, potentially, on why sector returns so often disappoint investors.

In the terminology of Kahneman and Tversky, any mining development can be viewed as a series of conjunctive events.

Once a mining company has demonstrated a mineral resource, it usually begins a trip down a well-trodden path toward production. Analytical studies of increasing sophistication, government and community approvals, funding, recruitment of qualified project managers, identification of customers, construction and operational commissioning are all necessary for success.

The omission of any single step in the sequence renders the whole incapable of completion. For a conjunctive business undertaking to succeed, each of a series of events must occur.

Kahneman and Tversky described how “people tend to overestimate the probability of conjunctive events and to underestimate the probability of disjunctive events”. A disjunctive event is where only one of a series of possibilities is needed for success.

Kahneman and Tversky observed that “even when each of these [conjunctive] events is very likely, the overall probability of success can be quite low if the number of events is large”.

Moreover, they concluded, “the general tendency to overestimate the probability of conjunctive events leads to unwarranted optimism in the evaluation of the likelihood that a plan will succeed or that a project will be completed on time”.

Timing is an important added dimension in the mining investment market context. Delays can jeopardise the willingness of investors to provide ongoing support.

Not only must each step along the development path be completed; it must be completed within a time-frame acceptable to investment markets to fully benefit those behind the funding.

In the context of a mining development, let’s assume there are seven necessary steps each of which has an 80% chance of success. Statistically, this is equivalent to drawing seven successive red balls from a bag containing eight red and two white balls, with replacement of the balls after each drawing.

The probability of the overall development being completed will be 21%.

The probability that just one step in the required mining project development sequence is not realised – the chance of drawing a white ball on any one of the seven draws – is 79%.

This example typifies the standard mining industry investment model. Investors are constantly being asked to back situations in which failure is the overwhelmingly most likely result.

Companies, when pitching for investors, will typically speak of each link in the development chain as having a high chance of success. In practice, this claim usually arises from other biased judgements.

The tendency to use historically favourable outcomes or those with which directors are most familiar to infer their own chances of success, while ignoring large numbers of failures, is another common decision-making bias.

Mining investment promoters are also inclined to apply the average chance of success attributed to each of the individual components to the overall outcome. On this reasoning, if each component of the plan has an 80% chance of success, the overall chance of completion is said to be 80%, despite the sloppy statistical analysis.

A disproportionate amount of mining industry investment is based on the “unwarranted optimism” arising from such decision-making biases.

Notwithstanding the strong empirical and theoretical evidence for the persistence of these errors, no attempt is made to control how companies present their investment propositions.

Most times, company executives will be entirely free to assert erroneously that the chance of success exceeds the chance of failure when the reverse will be true.

If executives had to attribute a probability explicitly to each event in the sequence they identify as being necessary to fulfil their production ambitions, they would gain a more realistic view about their projects’ worth.

Mining executives often lament publicly (and even more frequently privately) that markets do not share their expectations of success.

The reason for the disparity in views might be straightforward enough: executives are ignoring what Kahneman pointed out 40 years ago and what should be compulsory reading for any mining project promoter today. .