The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains but only after prices have already fallen by 70% or more in many cases leaving prices still historically low.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

Key Outcomes in the Past Week

The travails of Deutsche Bank were added to energy prices and expectations of changes in Federal Reserve policies as contributors to market movements.

Deutsche Bank more or less confirmed that the U.S. government had asked for US$14 billion as the price to settle outstanding regulatory infringements arising from the 2008-09 financial crisis and the use of mortgage securities.

Fears that such a payment would wipe out the bank’s remaining equity have contributed to a two thirds loss in market value since July.

The plight of Deutsche Bank highlighted the difficulty banks currently face, more generally, to rebuild capital while interest rates are so low and while regulatory pressures are forcing capital costs higher.

The bank’s subsequent indication that a settlement with the U.S. government may result in a fine as low as $5 billion improved sentiment about the sector and facilitated stronger markets more generally.

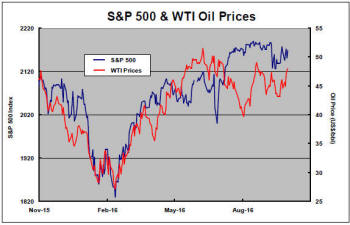

An improved oil sector outlook also helped the equity market. At a meeting in Algiers, the Saudi Arabian government appeared willing to concede market share to Iran to achieve a better oil price outcome. The breakthrough, after months of oversupply, will need ratification at a formal meeting of OPEC later in 2016 but the likelihood of fresh supply constraints appears to have risen. The parties to any agreement to place a cap on crude oil output do not include U.S. producers whose sensitivity to oil price movements could easily scupper any benefit. A rise in marginal U.S. production, encouraged by higher oil prices, could still offset cuts by Saudi Arabia.

Janet Yellen raised the prospect of the U.S. Federal Reserve buying equities to cope with a future economic downturn in a speech to bankers in Kansas City saying that it could be useful to act more directly on prices with a link to spending decisions.

The idea arose from a comparison between the powers available to the U.S. Federal Reserve and those of the central banks in Europe and Japan.

Legislation enabling the Fed to widen the scope of its powers would have to pass the U.S. Congress. With strong opposition among many members and senators to the Fed’s market interventions, often seen as bailing out Wall Street at the expense of ordinary Americans, the likelihood of the central bank widening its powers seems remote.

Meanwhile, expectations are solidifying around a Federal Reserve rate hike in December. A slight increase in the rise in the personal consumption price deflator to 1.7% (excluding food and energy) over the year ended August supported the expectation.

Markets also appeared to take support from the outcome of the first U.S. presidential debate between Hillary Clinton and Donald trump with the former Secretary of state appearing to get the better of her Republican opponent.

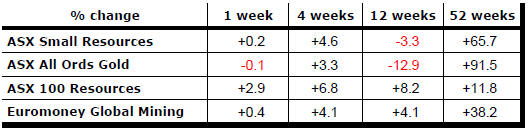

Within the resources sector, gold equities produced a negative return for the week as well as for the September quarter as the gold price tended to stabilise.

A more favourable risk environment, helped by the US dollar trading toward the low end of its range, has been favouring metal prices.

These conditions have attracted funds to the larger companies in the sector with the S&P/ASX 100 resources index adding 2.9% in the week and 8.2% in the quarter compared with returns of +0.2% and -3.3%, respectively, for the small resources share price index.

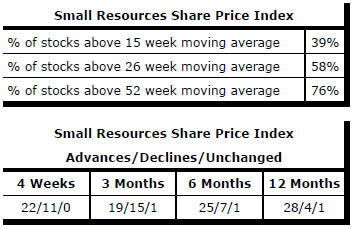

Market Breadth Statistics