The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

Key Outcomes in the Past Week

Market Breadth Statistics

Weakness in the U.S. dollar has persisted helping to boost earnings of U.S. international companies (and cutting back on the earnings of European multi-the nationals).

The currency move has supported U.S. dollar denominated commodity prices.

U.S. and emerging economy equity markets have both been strong with the latter outperforming most recently backed by greater optimism about the global growth outlook and improved commodity prices.

Higher industrial raw material prices have been evident across many (but not all) categories of products.

Among non-ferrous metal prices, nickel, tin, copper and lead have been especially strong recently while remaining more or less within the range occupied for the duration of 2017.

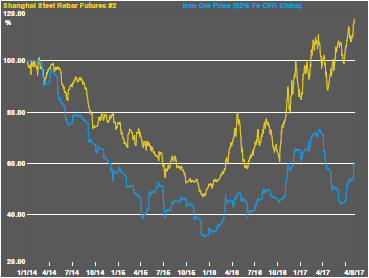

Rising Chinese steel prices have been reflected in iron ore price increases.

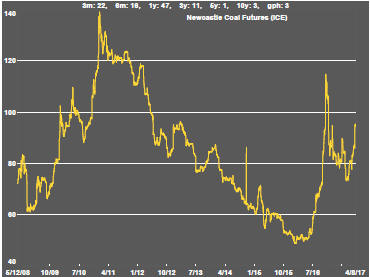

Coal prices also rose again in the past week.

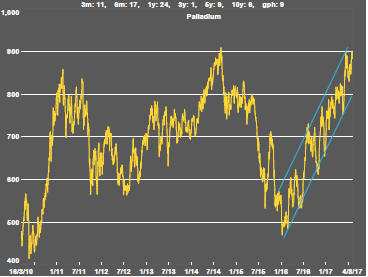

Among the precious metals, the uptrend in palladium prices persisted while underperforming platinum prices showed initial signs of breaking through a recent weakening trend.

Gold prices remained in a tug of war between bond yields and currency swings. The weaker dollar has helped push gold prices higher but lower bond prices have generally retarded price gains.

Silver prices remained more closely aligned with gold than palladium or, to a lesser extent, platinum.

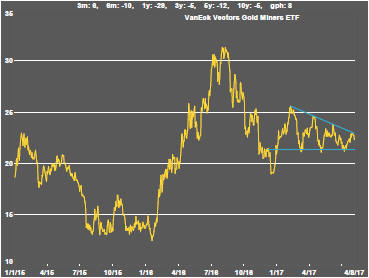

Gold-related equities have remained under pressure as a result of the subdued gold price momentum .

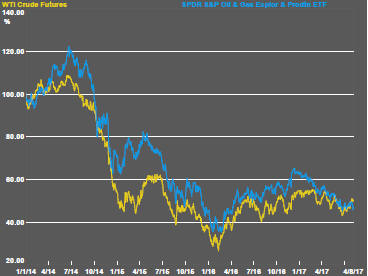

The oil and gas sector again proved weak with commentators increasingly referring to crude oil prices trading indefinitely within a tight band.

The uranium sector has quit its a long-term downtrend but shows little sign of recovery as it defines an increasingly prolonged cyclical trough.

.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.