The Current View

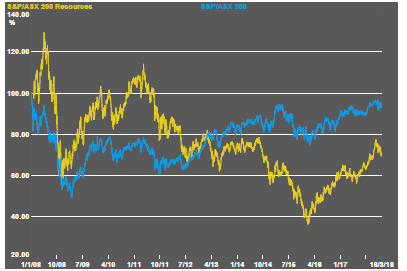

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

Resource Sector Weekly Returns

Market Breadth Statistics

Volatility perceptions have eased further, enabling equity markets to resume their upward bias.

Despite the emphasis on US economic and political events defining market outcomes, global markets remain correlated. Meanwhile, sectoral gains remain highly stratified.

Trade uncertainties have had a negative influence with the potential of tariffs or other trade impediments threatening to hinder continuation of recently higher rates of economic growth.

The appointment of well known economist Larry Kudlow to take a White House advisory role would have eased some market fears about the direction of policy but President Trump has also flagged, after the sacking of Secretary of State Tillerson, that there are more changes to come. Increasingly, this looks like the way the president prefers to conduct his business.

The Australian resources sector benchmark index has remained in weakening mode after having recouped the 2014-15 losses suggesting a lack of underlying impetus for a stronger revaluation of assets.

The inflation fears of a few weeks ago appear to have dissipated especially since the latest monthly US labour force statistics (for February) reverted to the long term pattern of strong employment gains with only modest wage increases.

In the coming week, new Federal Reserve chairman Powell will probably announce a hike in the Federal Funds rate. That widely anticipated move may prove less important than how the new chairman conducts the post meeting press conference which has become such an important communication device for the Fed while offering a chance for the chairman to trip up as he has to deal less formally with questions about the conduct of policy than in his carefully crafted written statement.

The meeting will also allow the release of the Fed governors' individual forecasts which will be scrutinised for hints about how frequently rates will be raised over the next 12 months.

The recent rise in bond yields has remained within the bounds of the decades long downtrend in yields. While downside expectations are limited, the absence of a break above the downtrend will have gone some way to ease tensions about the impact on equity prices of tighter monetary conditions. A break above trend may have more dramatic consequences.

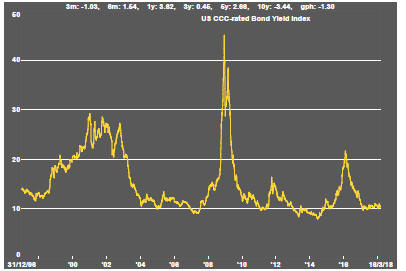

Low grade corporate bond yields have edged up slightly but, taken as a sign of financial conditions for miners, remain consistent with favourable funding conditions which have not deteriorated with the rise in market yields.

A slight upward bias in the US dollar has been the product of competing views about relative growth rates, fears about disruption to trade patterns and the funding requirement of the US government.

The newly legislated tax cuts and an omnibus spending bill tailored to get enough votes in both houses of the US Congress suggest longer term downside consistent with a history of a weakening currency occasionally punctuated by unsustained cyclical rises.

The gentle upward drift in the Australian dollar could remain intact as long as risks to global economic conditions remain lowered and commodity prices are in the upper end of the range of prices in the past year. Within that trend, tightening monetary conditions in the USA and, later, in Europe could exert more downward pressure as they occur.

In the near term, trade disputes between the USA and its major trading partners in Canada, Mexico, Europe, Japan and China could add headwinds for any country potentially caught in the crossfire, including Australia.

The general upswing in commodity prices over the past year remains within the bounds of a cyclical trough suggesting still stronger economic activity will be needed to carry prices higher.

The gold price has been subjected to a tug of war between the negative effect of higher bond yields and the positive influence of a weaker US dollar.

Threats to world trade patterns would have added some upward bias to prices which have now moved markedly out of line with the change in bond prices.

The net change in bullion prices has been relatively modest despite the sometimes unusually large swings in macro variables.

Prices of Australian gold related stocks have moved within a narrower range than their north American counterparts. Australian prices sit around the upper end of the range of outcomes over the past year. In contrast, North American prices are around the lower end of their range.

Both groups of stocks have shown less than historical leverage to higher bullion prices. The North American stocks have shown the stronger connection to financial market conditions over the past month.

Within the precious metal complex, palladium prices remain well ahead of relatively stable gold, silver and platinum prices despite the upward move facing the strongest headwinds in over a year.

Prices of the main daily traded nonferrous metals had become increasingly correlated with a broadening consensus about the lowered risks to world economic activity.

Tin prices have lagged conspicuously over the past year but showed a similar rise to that of other metals (and a more recent decline) since late in 2017.

All prices have tended lower as concern about disrupted international trade patterns have intensified and as (still minor and ambiguous) signs of weakness in Chinese activity rates have had an effect.

Bulk commodity price tipped lower in the past week.

Demand for iron ore has remained at cyclically high levels but with little change over the past four years in global steel production, the scope for significant tightening in market conditions is more limited than for coal.

The coal market will have been a beneficiary of increasingly constrained supplies with capacity being closed in Asia and development plans elsewhere under threat despite rising demand from energy suppliers and steel producers.

In a similar reaction to that evident among the gold stocks, equity prices for oil and gas explorers have been dominated by broader stock market movements rather than movements in the price of crude oil.

Higher US production remains a burden on investor expectations.

Eighteen months of rising lithium stock prices has given way to a period of market reassessment as a lengthy pipeline of potential new projects raises the prospect of ongoing supplies being adequate for expected needs.

Potential lithium producers have been able to respond far more quickly to the various market signals than has been the case in other segments of the mining industry.

Battery metals remain a focal point for investors with recent attention moving to cobalt and vanadium.

Uncertainty over how a peaceful transfer of power can occur in the Democratic Republic of the Congo has added a dimension to cobalt prices lacking in other metals caught up in the excitement over transport electrification.

The uranium sector is once against moving along the bottom of its long time trading range in the absence of more meaningful signs that power utilities are prepared to re-enter the contract market to negotiate their longer term needs.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.