The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

Key Outcomes in the Past Week

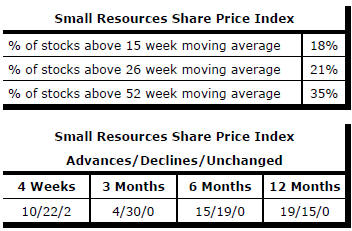

Market Breadth Statistics

The correlation between gold bullion prices and the prices of gold-related equities had fallen to unusually low levels in the past fortnight. The chart shows a moving 40 day correlation between the gold price and the Van Eck junior gold miners exchange traded fund.

In the shorter term, equity prices are highly leveraged to changes in gold bullion prices. A 10% change in the gold price over the course of a month has been associated with a 19% change in equity prices during 2009-17.

Since the end of January 2017 and contrary to the historical trend, the gold price has risen by 3.2% while the equity prices have fallen by 13.7%.

The relative movements are suggestive of some catch-up potential among gold related equities if the price of gold is able to sustain current levels.

U.S. 10 year bond yields rose through 2% in the immediate aftermath of Donald Trump’s election as U.S. president but, since December, have edged lower (and bond prices have moved higher).

While on the campaign trail Trump spoke about the U.S. economy growing by as much as 4%. Such an outcome is currently unrealistic. Even getting to 3% for an economy struggling for years to reach 2% will prove challenging and require fresh policy initiatives.

For the time being, bond yields appear broadly consistent with an economy expanding at a nominal rate of 3-3.5%.

At the same time, the U.S. dollar has been tending lower as judgments about interest rate rises are tilting toward a view that there may be fewer than Federal Reserve members had been anticipating.

The prospect of more moderate U.S. growth outcomes is also reducing the attractiveness of the U.S. economy as an investment destination.

The combination of bond prices stabilising at relatively high levels and a U.S. dollar tending lower is supporting the gold bullion price for the time being.

Moves to reduce taxation and lower business regulations are likely to disrupt this favourable combination but this effect will most likely be delayed until markets regain confidence about President Trump’s policy effectiveness.

To the extent these conditions persist, there will be a window of opportunity for gold related equities to make up their relative performance losses.

.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.