The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

Key Outcomes in the Past Week

Market Breadth Statistics

The key U.S. market indicators again hovered around or pushed to new record levels.

Of particular note has been the relative strength of the Russell 2000 index which suggests a stronger appetite for risk among investors.

Another contributor to the performance of the index comprising smaller more domestically oriented companies than those in the S&P 500 will have been a more optimistic view of U.S. economic growth, helped by expectations of lowered corporate tax rates.

The lowered volatility implied by option prices has been consistent with the index outcomes and the greater willingness to buy risk.

The divergence in S&P 500 sector performance has begun to erode insofar as the worst performing sectors have attracted more investor interest.

The stronger performance of the previously lagging energy and telecommunications sectors is a sign that investors are not buying indiscriminately but are conscious of relative prices and valuations in taking the overall market higher.

The previous divergence in performance is now permitting a more prolonged rise in overall indices than might have otherwise been the case.

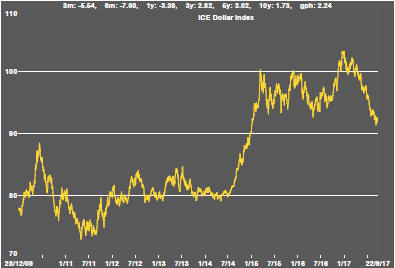

The fall in the U.S. dollar stalled slightly in the past week as the currencies of major U.S. trading partners retreated slightly from their recent gains.

Base metal prices tended to give up their recent gains, in line with the loss of exchange rate momentum, although aluminium prices again stood out for their relative strength.

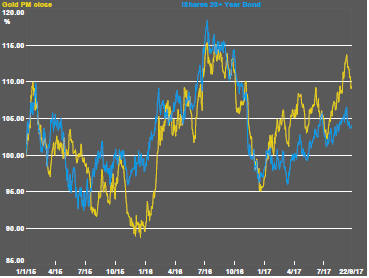

Gold bullion prices turned lower as U.S. government bond prices fell and as the U.S. dollar proved less supportive than it had been in recent weeks.

Precious metal prices were generally lower - matching the decline in gold prices. Palladium prices have remained within a lengthy uptrend but the force of the prior rise suggests a high risk of something lower in the immediate future even as the uptrend remains intact.

Gold-related equity prices responded as one would expect to the lower bullion prices.

Gold-related equity prices have not displayed significant leverage to the stronger bullion market outcomes through the course of 2017 and appear to have discounted the longevity of the metal price rises which have occurred.

Equity investors appear to be putting more emphasis on positive U.S. growth outcomes which would also suggest higher bond yields and a stronger U.S. dollar, both of which would have an adverse impact on gold prices.

A more bullish tone in crude oil markets has been accompanied by an upward break in the prices of oil and gas exploration stocks.

Iron ore prices have lost momentum and have failed to participate in the exchange rate induced price recovery experienced by a range of nonferrous metals.

.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.