The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains but only after prices have already fallen by 70% or more in many cases leaving prices still historically low.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

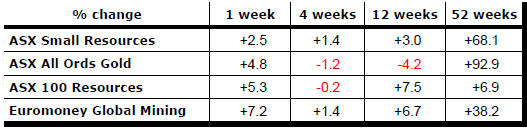

Key Outcomes in the Past Week

Oil price swings and speculation about Federal Reserve policies continued to dominate market outcomes in the absence of strong trends in growth.

Some improvement in metal prices supported resource sector equity values with the key sector indices showing gains for the week. The largest stocks benefitted most.

An OPEC initiated meeting in Algiers in the week ahead had raised some hopes of a price-support agreement. Saudi Arabia had appeared to be willing to accept a production cut but any action remains dominated by strategic tensions between Saudi Arabia and Iran.

Iran has been inching closer to its targeted production rate of four million barrels of oil per day raising hopes that it would be willing to agree to a pause in the output expansion. At the end of the week, this appeared less likely than at the beginning.

As widely expected, the U.S. Federal reserve did not raise its Fed Funds rate although it hinted strongly that a rate rise would occur when policymakers meet in December. Unusually, three members of the committee formally disagreed with the decision.

At the same time, committee members have pulled back their expectations of the pace of subsequent rate rises. Their modified forecasts eased some of the fears among traders that future rises might prove too aggressive for an economy still growing at less than 3%.

The Bank of Japan also met in the week amid expectations of fresh initiatives to achieve its 2% inflation target.

In opting for a bond yield target in place of its previous asset purchasing objective, some thought Bank of Japan policymakers had recognised the limited impact they were having on inflation. Subsequently, a bank spokesperson said that the changed target would not cause an imminent change in the volume of purchases.

Some will be pleased that the bank may have recognised its limitations but, more worryingly, the bank’s concession may simply reflect a more general impotence among central banks about their abilties to affect economic outcomes.

Statistics from the UK appear to show a less severe economic impact from the vote to leave the European Union than had been feared although business groups continue to forecast an investment cutback.

While potentially lesser disruption from the UK exit from Europe would remove one global growth risk, the World Trade Organization and the OECD have both added to the warnings from the International Monetary Fund that a contraction in world trade growth is now damaging the overall output growth picture.

Market Breadth Statistics