The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

Key Outcomes in the Past Week

Market Breadth Statistics

Markets remained near record levels but a loss of momentum is evident.

Greater attention to the detail of the Trump economic plan has resulted in divergent views about outcomes including the nature of health care and taxation policies and the timing of any likely changes.

Markets are bracing themselves for the unexpected. New president Trump's decision to change immigration policies, for at least the short term, highlighted the extent to which policymaking was changing.

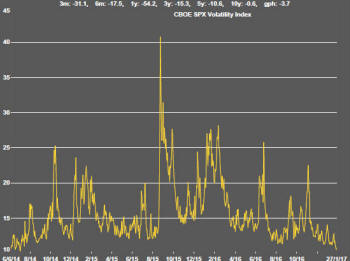

In pushing still lower, the volatility index based on S&P 500 option prices suggests a market with few concerns among investors about direction although the extremely low VIX reading also highlights a market vulnerable to be even modest reversals in sentiment.

Some of the more strident statements from the new Trump administration about trade policy have raised the prospect of damage to US export performance.

The potential damage to North American supply chains became a greater worry as relations between Trump and his Mexican counterpart appeared to break down when a scheduled meeting between the two was canceled.

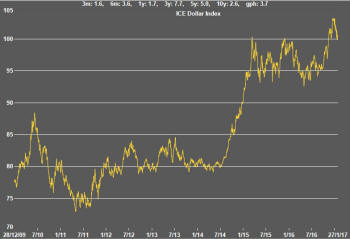

Exchange rate movements are becoming more susceptible to Trump policy initiatives (with a loss of Federal Reserve influence).

Key commodity prices have lost their upward momentum for the time being although the largest companies in the sector continued to benefit from recent gains.

The largest stocks in the sector are benefitting from reallocations of funds by professional money managers in response to changed perceptions of risk against a background of recent commodity price improvements.

The positioning of smaller stocks in the sector is more ambiguous.

Falling volatility shown in the third chart in the right hand panel suggests higher prices are feasible.

The relationship between the small resources share price index and high yield bond prices illustrated in chart 6 also suggests higher equity prices are possible.

Against these two indicators, measures of relative strength are showing a loss of momentum leading to a rising chance of a near term decline in prices or, at least, a struggle to break through those levels which had prevailed in the first part of 2015 before the last leg down in sector prices.

Uranium sector stocks continued their upward bias with renewed interest from investors. Some small capitalisation companies are displaying especially strong leverage to a still modest improvement in reported spot uranium prices.

The strong link between gold bullion prices and movements in US government bond prices has persisted leaving gold price outcomes biased to the downside at least as long as expectations of a growth rebound in the USA as a result of new policies from the Trump administration prevail.

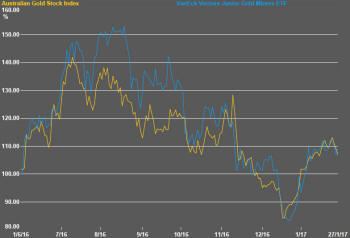

Australian gold equity price movements have closely matched those of their north American counterparts.

.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.