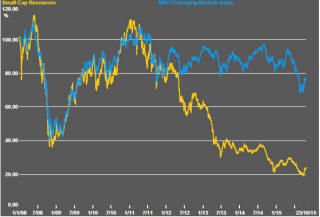

The Current View

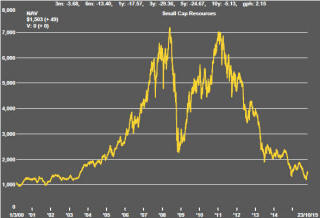

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments. The market is now entering a period prone to even greater disappointment about project delivery .

Has Anything Changed?

The assumption that June 2013 had been the cyclical trough for the market was premature.

Sector prices have adjusted to the next level of support. The parallel with the 1990s illustrated in Chart 4 is being tested. Prices will have to stabilise around current levels for several months for the thesis to hold.

Key Outcomes in the Past Week

Equity markets continued to make gains during the week after the sell-off in August and September which occurred following mounting concerns about China’s economic outlook.

The last leg of the 2% gain in the S&P 500 for the week occurred after China had again taken steps to shore up its economic outlook. On this occasion, the Japanese and European central banks had also been flagging additional stimulus measures and doubts had arisen about whether the Federal Reserve would proceed with an interest rate increase in 2015. Overall, the outlook for policy induced asset price inflation was looking rosier.

By the end of trading on Friday, the S&P 500 had recovered all but 27 of the 234 point loss it had suffered in August. As usual, slightly over 70% of the S&P 500 companies have reported better than expected earnings for the September quarter although, also as usual, this has come after expectations have been managed down and, on this occasion, without a positive revenue contribution.

Improved U.S. market conditions have been narrowly based with a handful of high profile technology stocks having driven the market higher while a majority of companies continue to display poor share price momentum.

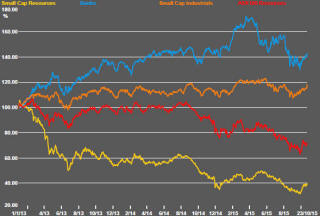

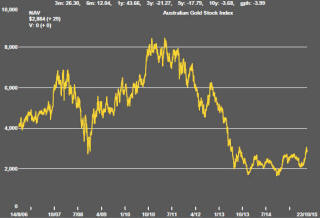

The resource sector also lost momentum although the smaller companies in the sector maintained the comparative performance advantage which has become evident in recent weeks. The small resources share price index increased 1.4% over the week. The S&P/ASX 100 resources index fell 0.4%. The Euromoney Global Mining Index gave up 1.2%.

The possibility that the European central bank would maintain is easy money policy for longer than had previously been foreshadowed just as the U.S. Federal Reserve was winding back its stimulus created renewed upward pressure on the U.S. dollar exchange rate after several weeks in which the currency alignment had stabilised. The stronger dollar added downward pressure to U.S. dollar denominated metal prices.

The focus on global growth is likely to remain in the coming week as Federal Reserve policymakers meet again in Washington and Chinese leaders gather in Beijing to put the final touches to their economic plan for the upcoming five years.

China Moves Again to Boost Growth

The Chinese central bank has announced a 25 point cut in its benchmark 12

month lending rate to take to six the number of rate reductions since

January 2015. The Chinese central bank is one of the three majors with its

counterparts in Japan and Europe to have flagged a willingness to provide

more monetary stimulus to help spur growth in their ailing economies.

The stock market reaction to this rate cut has been more favourable than reactions to the steps taken by the Chinese government in August after which market volatility rose dramatically resulting in a fall in value in all major equity markets.

On this occasion, markets have apparently concluded that the prospect of additional stimulus from China, Japan and Europe will benefit markets. On the prior occasion when markets drew a more pessimistic inference, the fresh policy measures were taken to mean economic conditions were worsening.

A single rate cut of the magnitude announced on Friday is unlikely to make much difference on its own to growth leaving markets still susceptible to further negative reactions when, almost certainly, further policy measures will be needed to help supplement the growth momentum.

. .

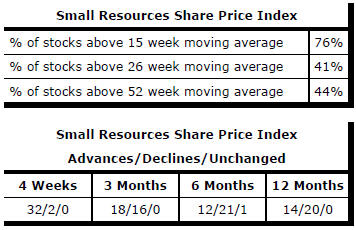

Market Breadth Statistics